Publication date: September 4, 2025. The information in this guide is accurate as of this date. If and when we make wholesale, material updates, we will update its publication date.

Whether you're just browsing or ready to make a move, buying a home comes with a lot of questions.

To get the answers that matter most, tell us which stage you’re in:

> 5 years out

Planning

ahead

< 5 years out

Thinking

it through

This year

Ready

to go

Or dive straight into the full guide below

What are the all-in costs of home ownership?

Conventional wisdom may lead you to believe that the only costs of home ownership are the down payment and

the monthly mortgage payment. However, if you budget with only these two factors in mind, you'll likely be

caught off guard when the bills come rolling in.

Some additional costs to keep in mind:

This cost breakdown is not meant to discourage you from exploring homeownership. Rather, this information

should help you better anticipate the costs you can expect when you become a homeowner.

See the benefits of home ownership

What does it take to qualify for a mortgage?

When it comes to securing a mortgage, there are several financial factors at play.

Here are a few things you can do to ensure you qualify for a mortgage with favorable terms:

Keep your credit score up

Mortgage lenders consider your credit score when determining how risky it is to give you a loan, which impacts

the interest rate you can get. All else equal, if your credit score is above 760, you are likely to get a

mortgage interest rate that is about 0.25% to 0.375% lower than someone with a credit score of 660. If your credit

score is in the 500s, you should expect some challenges in qualifying for a mortgage and, if you do find one, it

may have a much higher interest rate.

Keep your debt-to-income (DTI) ratio low

Your DTI is the sum of all of your monthly debt payments, including credit lines, minimum monthly payments for

any credit card debt, auto loans, and your upcoming mortgage expenses, as a percentage of your monthly pre-tax

income. Most mortgage lenders prefer to issue a mortgage that will keep your DTI below 40%. Once your DTI goes

above 43%, it becomes much more difficult to secure a mortgage.

Make a healthy down payment

The size of your down payment, or the upfront payment you make on the house, impacts your interest rate, whether

you need to pay private mortgage insurance, and the size of your monthly mortgage payments. Conventional wisdom is to

put at least 20% down to avoid the need for mortgage insurance, but there are various loan options that allow

for a down payment as low as 3%. On average, first-time homebuyers put about

9% down.

In general, the bigger your down payment, the lower your interest rate.

While your home budget is limited by the size of your mortgage, other factors are at play as well when it comes to affordability.

See more details

How big should my down payment be?

Before diving into the details, let's first define a few key terms:

Down payment refers to the upfront payment you make on the house.

Principal payments reduce the amount you owe on your mortgage.

Interest payments are what the bank charges for lending you the money.

The size of your down payment directly affects the overall costs of your home. The more you put down, the

smaller your loan amount, and thus the smaller your monthly principal and interest payments will be, all else

equal. You should also know, however, that lenders will typically give you a better interest rate the more you

put down. If you put less than 20% down, you will typically need to pay for mortgage insurance. Conventional

wisdom is to put at least 20% down to avoid the need for mortgage insurance, but there are various loan options

that allow for a down payment as low as 3%. On average, first-time homebuyers put about 9% down.

Larger down payment means lower monthly payments

The example assumes a single-family home that costs $800,000 with a 30-year fixed rate mortgage. It also assumes the buyer has a 760 credit core with a 25% DTI ratio.

Down payment

10%

20%

30%

Monthly principal and interest payment

$4,521.57

$4,013.30

$3,469.17

Monthly mortgage insurance

$90

$0

$0

Total monthly costs

$4,611.57

$4,013.30

$3,469.17

Note: Assumes 6.438%, 6.424%, and 6.308% interest rates respectively for 10%, 20%, and 30% down payment scenarios.

When is the best time to buy?

Timing the real estate market is like trying to time the stock market––it’s very hard to do. Home prices will go

up and home prices will go down. Plus supply and demand varies regionally, making any attempt to time the market

even more challenging.

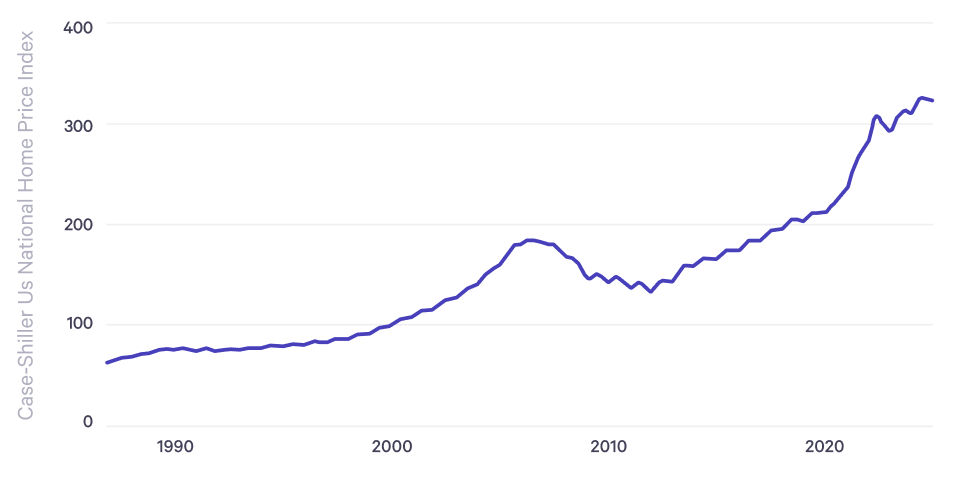

As evident from the Case-Shiller Home Price Indices, a leading measure of US residential real estate prices,

while home prices in the US have increased over time, real estate market volatility is hard to avoid.

Keep in mind there’s also an implicit cost to waiting. Even if you don’t move forward with buying a home, that

doesn’t mean you’re not incurring housing expenses. For instance, waiting a year to buy a home means paying a

year of rent to your landlord instead of building equity in a home.

Find out how to compare renting versus owning.

What if there's a market downturn?

Unfortunately, if the real estate market declines, so will the value of your home. On the other hand, if the

real estate market rises, homeowners will benefit from the appreciation of their home value. Just like financial

markets in general, the only sure thing in the real estate market is that it will go up and it will go down.

The market is unpredictable

The impact of volatility in the real estate market is unavoidable, even if you’re not a homeowner. If you rent

and the real estate market is on the rise, you can surely expect your rent to increase. But rent prices do not

always increase one-to-one with home prices.

In the event of a downturn, if you have a fixed-rate mortgage your monthly mortgage payments should not be

affected by any market volatility. However, you may be at risk if there’s a significant drop in real estate

prices and you have a sudden need to sell your home, say for a job opportunity in a new

location. In this case, you may be forced to sell your home at a loss. If the value of your home has decreased

significantly, you may not have enough to repay the remaining balance on the mortgage. In general, the larger

your down payment, the lower the risk that you face this particular issue.

Don't be discouraged by uncertainty

It’s wise to understand what can potentially go wrong. But in the face of certain uncertainty, our home-buying

philosophy is the same as our philosophy about investing: The risk of a downturn is a part of life. Having a

long-term time horizon, staying the course, and not using too much leverage is your best path forward.

Consider the benefits of owning a home.

How does location factor in?

Deciding where to buy is often almost as big of a decision as which home to buy. For those living in urban areas

like New York or San Francisco, a fairly common question that arises is whether or not to make the move to the

suburbs.

A major draw of the suburbs is you can sometimes get a larger home for the same budget. But, on the other hand,

there are many perks and conveniences of city life that can’t be easily replaced when you move away. This is

worth considering when you work through the decision to buy a home.

Aside from size of home you can get for your money, there are a number of other factors to consider and

trade-offs to think through when deciding on the location to buy that's right for you:

Property taxes

Property taxes can vary dramatically by city or county. According to the

Tax Foundation,

some states have property tax rates of over 2%, while others are under 0.50%

Mortgage rates

The location you choose may affect the interest rate on your mortgage. Lenders factor in the difficulty of

selling a home given its location in case of foreclosure.

School

If you are planning on starting a family or have kids now, school districts are another major factor in

deciding where to live. Great public school districts often increase home prices in a specific area, which

means you may have to pay a premium for access to better education.

Commuting

If your job is in the city, moving to the suburbs will mean increased time and money spent traveling every day.

Living costs

The cost for groceries, utilities, and other services can also vary widely between urban and suburban areas.

What are the benefits of owning your home?

Practical

Even if you don’t buy a home, you still need to pay something for lodging. For most people, this is in the form

of monthly rent. When you buy a home and pay a mortgage, you’re actually saving into a permanent asset. Plus,

you get automatic protection against rising rent costs.

See how to value a home as an asset

Economical

Owning your home comes with a few potentially significant tax breaks. While you don’t get a tax deduction for

paying rent, as a homeowner you can deduct the interest you pay on up to $750,000 of your mortgage balance and

up to $40,000 in property taxes. When it comes time to sell your home, you can exclude capital gains up to

$250,000 (or up to $500,000 if you file a joint tax return with your spouse).

Emotional

The most significant benefits to owning your home are likely not financial. You want to buy a home because you

want a place to call your own, a place that gives you freedom to live the life you want. Your reasons are often

justifiably emotional, which is why the case for buying a home can’t simply be rationalized by a financial

model.

How should I value my home as an asset?

The costs of homeownership can be a huge portion of your monthly expenses. But over time your house could also

become one of your largest assets. As you start paying down the principal on your mortgage, you also start

building home equity, or the amount of ownership of your home. If you decide to sell your

home in the future, you will likely have cash on hand to spend on something else.

A useful formula to remember:

Home equity = current home value - current mortgage balance

Example

Home equity builds over time

On day 1, you make a $100,000 down payment on a $500,000 home.

In year 5, you’ve paid down just over $23,000 in principal (assuming a 30-year 7.00% fixed-rate mortgage), so

now you owe a bit over $377,000. And let’s imagine the value of your home has appreciated to $564,000.

A few risks to keep in mind

While a home has value, there are a few considerations to keep in mind that may affect the amount of cash you

can expect from a future sale of the home. First, the real estate market fluctuates and is unpredictable. If

the market goes up, so does the value of your home. Of course, if the market goes down, your home value will

also decrease.

See more on how to think about the real estate market.

In addition, when it comes to selling a home, keep in mind that real estate commissions, home improvement

efforts, transfer tax, and moving costs can add up to

over 10%

of the total sale price.

How do I compare buying versus renting?

When it comes to home ownership, it's tempting to compare your monthly rent with your potential monthly

mortgage. While this is a logical way to evaluate costs on a monthly basis, it actually ignores a number

of significant considerations.

The right monthly costs comparison

To make an accurate comparison between renting and owning, you should understand the full costs of

homeownership. In addition to monthly mortgage payments, there are a number of additional monthly home expenses

to consider, such as property taxes, insurance, and HOA fees. These other expenses can add significantly to your

total monthly costs.

Review the all-in costs of homeownership.

Buying requires upfront payment

In order to be approved for a mortgage, you will need to make a down payment. Putting at least 20% down lets you

avoid mortgage insurance, but there are loan options with as little as 3% down. The average first-time homebuyer

puts about 9% down. In addition, the amount of down payment you make affects the terms of your mortgage.

See what you should know about the down payment.

Equity in your home

While buying requires more upfront costs, you also own the house outright, albeit with debt from the mortgage.

Over time, the monthly mortgage payments you make will start increasing your home equity. The money you pay on

rent, on the other hand, is money you'll never get back.

See how to value a home as an asset.

What can I do today to be prepared?

If a home purchase isn't in your immediate future, there are a few things you can do to better prepare

far in advance.

Pay down any debt

When you pay down your debt, you decrease your debt-to-income ratio. This is a key input in determining the

terms and interest rate for your mortgage. As a rule of thumb, we suggest keeping your debt-to-income (DTI)

ratio below 43%.

See more details about mortgages.

Improve your credit score

Lenders use your credit score to assess the risk they take on when giving you a loan. They use it to determine

whether you qualify for a mortgage and what interest rate you’ll pay. A healthy credit score is 740 or higher

and you’ll get the best interest rates with a 780 or above. To increase your score, monitor it via credit

reports, set up bill payment reminders and pay down any debt.

Source: “How to repair my credit and improve my FICO scores”

by My FICO.

Save intentionally

This might seem like a no-brainer, but everyday expenses can get in the way of proactively saving for larger

goals. By defining a monthly amount to put towards a home and depositing it in an appropriate savings or

investment account, your future won’t become an afterthought.

Learn more about how to invest home savings.

Time can be your friend. A longer time horizon means more time to save for your down payment and build up your

credit score. However, just because you’re buying more time to save for a home purchase doesn’t mean you don’t

have living expenses. Be sure to factor in rent and other household expenses into your savings plan.

How does a home fit in with my other goals?

The right home is one that still allows you to meet your other financial priorities with confidence.

This means understanding how much home you can afford, and also having a clear sense of your other

goals — both short and long term.

Start on the right foot

Before you start saving for a home, consider putting money towards paying down high interest loans. There are

differing opinions about what constitutes a “high interest loan,” but as a rule of thumb, you might want to

consider paying down loans with interest rates greater than 8%, such as credit card debt.

Next, consider contributing to your company-sponsored 401(k) if your employer offers a matching contribution. An

employer match is basically free money, making it much more attractive to participate.

Map out your priorities

After you pay down debt and put money towards your 401(k), it's time to understand what your financial

priorities are. Do you want to cover your children's college education costs in full? What about having a

comfortable lifestyle in retirement? Do you need to buy a home sooner than later? Once you've decided the

relative importance and timing of these priorities, you can then determine how much of your savings to allot

to each goal.

Understanding the trade-offs

The reality is you only have so much money to work with, so prioritizing one goal will have an impact on the

others. To illustrate how to consider tradeoffs, let’s walk through a very simplified example. Let’s say you’re

deciding between buying a larger home that costs $800,000 or a more modest home that costs $500,000.

How should I invest my home savings?

There are several ways to invest in the funds you've set aside for a future home purchase.

The right option for you, depends on your time horizon.

Within five years

Markets can be volatile from year to year. In fact, our analysis shows that there could be a

25.2% probability of loss

for investments held for just one year. For near-term home purchases, it’s more prudent to stay out of the

markets to avoid a potential downturn. If your home purchase is in the next five years, consider investing funds

for a down payment in a lower-risk option, such as a high-yield savings or cash account (like the

Wealthfront Cash Account), fixed income (like Wealthfront’s

Automated Bond Ladder

or

Automated Bond Portfolio), certificates of deposit (CDs), or a money market account.

More than five years away

If your time horizon is longer, your savings can afford to take on more risk. For home purchases that are more

than five years away, consider investing your money in a long-term diversified investment portfolio, which can

deliver higher returns than short-term savings options. As you get closer to purchasing a home, we suggest

moving that money from your investment account to a safer, low-risk option, as mentioned above.

Consider investing your long-term savings with Wealthfront.

When you’re buying a home, getting a low mortgage rate can save you thousands.

Are you a prospective home-buyer in CO, TX, or CA? Soon, Wealthfront will offer a simpler way to get a great rate. Join our waitlist to stay in the loop.