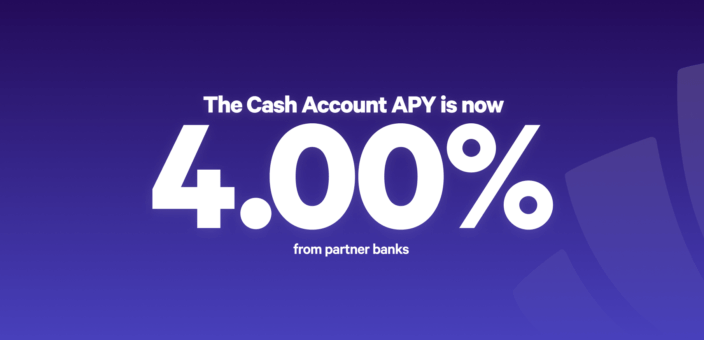

On Wednesday, December 18, the Federal Open Market Committee (FOMC) lowered the target range for the fed funds rate by 0.25% because of continued progress against inflation. As we’ve written about in the past, the fed funds rate is a direct input to the Cash Account Annual Percentage Yield (APY). As a result of the Fed’s decision, the new APY is 4.00%.

This new APY is nearly 10x the national average, which means the Cash Account is still an ideal home for your cash until you’re ready to invest. In addition to the high APY, we offer up to $8 million of FDIC insurance through our partner banks with no monthly fees, ever. The Cash Account also comes with many ways to conveniently access your cash, including free instant withdrawals, a debit card, compatibility with apps like Venmo & Apple Pay, the ability to send checks for free, and free wire transfers. You can access 19,000+ free ATMs, and we’ll reimburse up to two out-of-network ATM fees per month. You can even use your account and routing numbers to pay bills like your credit card, daycare, and mortgage.

We know that changing interest rates might make you wonder how to make the most of your savings in the current market conditions. We wrote a blog post to help you navigate the current interest rate environment.

Why is the APY going down?

The APY is highly dependent on the fed funds rate, which is the interest rate at which banks lend each other money, and the basis for most consumer interest rates. Wealthfront is not a bank, so we work with partner banks where we broker your Cash Account deposits. Those partner banks pay a rate based on a premium relative to the fed funds rate. When the federal funds rate goes up, we are able to raise the APY as we did several times in 2022 and 2023. On the other hand, it also means that when the fed funds rate declines, the APY also declines. You can rest assured that we’ll continue to navigate relationships with our partner banks so you can benefit from a competitive APY in all rate environments.

An ideal home for your short-term savings and everyday cash

At Wealthfront, we want to help you build long-term wealth on your own terms. We’re proud to offer a Cash Account that allows you to earn more interest on your deposits so your cash can grow faster with no extra effort, no monthly fees, and no market risk. The Cash Account is an ideal home for your everyday cash and short-term savings until you’re ready to invest, and it comes with best-in-class automation features so you can organize your savings into categories, track your progress against your goals, and invest your money within minutes during market hours. Best of all, the Cash Account just keeps getting better. Stay tuned for more improvements to our Cash Account in 2025.

Don’t have a Cash Account yet? You can sign up for one here.

Disclosure

Cash Account is offered by Wealthfront Brokerage LLC (“Wealthfront Brokerage”), a Member of FINRA/SIPC. Neither Wealthfront Brokerage nor any of its affiliates are a bank, and Cash Account is not a checking or savings account. We convey funds to partner banks who accept and maintain deposits, provide the interest rate, and provide FDIC insurance. Investment management and advisory services–which are not FDIC insured–are provided by Wealthfront Advisers LLC (“Wealthfront Advisers”), an SEC-registered investment adviser, and financial planning tools are provided by Wealthfront Software LLC (“Wealthfront Software”).

The Annual Percentage Yield (APY) for the Cash Account is as of November 15, 2024, and may change at any time, before or after the Cash Account is opened. No minimum balance required. The APY for the Wealthfront Cash Account represents the weighted average of the APY on the aggregate deposit balances of all clients at the program banks. Deposit balances are not allocated equally among the participating program banks.

The cash balance in the Cash Account is swept to one or more banks (the “program banks”) where it earns a variable rate of interest and is eligible for FDIC insurance. FDIC insurance is not provided until the funds arrive at the program banks. FDIC insurance coverage is limited to $250,000 per qualified customer account per banking institution. Wealthfront uses more than one program bank to ensure FDIC coverage of up to $8 million for your cash deposits. For more information on FDIC insurance coverage, please visit www.FDIC.gov. Customers are responsible for monitoring their total assets at each of the program banks to determine the extent of available FDIC insurance coverage in accordance with FDIC rules. The deposits at program banks are not covered by SIPC.

“Nearly 10x national average” is based on https://www.fdic.gov/national-rates-and-rate-caps as of December 16, 2024, for the national average interest rate for savings accounts.

We’ve partnered with Green Dot Bank. The checking features offered on your Wealthfront Cash account are provided by and the Wealthfront Visa® Debit Card is issued by Green Dot Bank, Member FDIC, pursuant to a license from Visa U.S.A. Inc. Visa is a registered trademark of Visa International Service Association. Checking features for the Cash Account are subject to identity verification by Green Dot Bank and the Wealthfront Visa® Debit Card is optional and must be requested. Wealthfront products and services are not provided by Green Dot Bank. Green Dot Bank operates under the following registered trade names: GO2bank, GoBank and Bonneville Bank. All of these registered trade names are used by, and refer to, a single FDIC-insured bank, Green Dot Bank. Deposits under any of these trade names are deposits with Green Dot Bank and are aggregated for deposit insurance coverage.

Fee-free ATM access applies to in-network ATMs only. For out-of-network ATMs and bank tellers a $2.50 fee will apply, plus any additional fee that the owner or bank may charge. Fees and Eligibility requirements may apply to certain checking features, please see the Deposit Account Agreement for details. Copyright 2024 Green Dot Corporation. All rights reserved.

The domestic out-of-network ATM fee reimbursement program (the “Program”) allows Wealthfront Brokerage clients with open and funded individual Wealthfront Brokerage Cash Accounts (“Cash Account”) who have requested and received an accompanying debit card (“Debit Card”) issued by Green Dot Bank (“Green Dot”) to be eligible for certain account benefits when using their Debit Card for a domestic out-of-network ATM cash withdrawal of U.S. dollars (“ATM Transactions”) when their Wealthfront accounts, Green Dot accounts (collectively, “Accounts”), and Debit Card remain open, active, and in good standing.

Each calendar month, current eligible clients with ATM Transactions will receive a reimbursement of certain fees associated with their first two ATM Transactions. Wealthfront Brokerage will utilize its best efforts to reimburse Green Dot’s $2.50 “out-of-network fee” and up to $5.00 of any operator or owner’s fee for your ATM Transactions, up to a maximum reimbursement of $7.50 per ATM Transaction (the “Reimbursement”). Your maximum total monthly Reimbursement shall be $15.00 ($7.50 + $7.50). If an ATM operator charges fees other than out-of-network fees and/or owner’s fees, Wealthfront Brokerage will not reimburse any portion of those fees. Once the maximum total monthly Reimbursement has been reached, no subsequent out-of-network ATM fees or charges that occur that calendar month will be reimbursed. ATM Transactions completed before September 16, 2024 shall not be eligible for Reimbursement in connection with this Program. Wealthfront Brokerage reserves the right to modify or terminate the Program at any time without notice. For full details please review the Out-of-Network ATM Fee Reimbursement Terms and Conditions.

Please note, Real-Time Payments (RTP) transfers may be limited by destination institutions, daily transaction caps, and by participating entities such as Wells Fargo and the RTP® Network. New Cash Account deposits are subject to a 2-4 day holding period before becoming available for transfer. Wealthfront doesn’t charge for transfers, but receiving institutions may impose an RTP fee.

Wealthfront does not charge for wire transfers, however receiving or sending institutions may impose a fee. For more information about wires, visit https://www.wealthfront.com/legal/online-transfer-agreement

The information contained in this communication is provided for general informational purposes only, and should not be construed as investment or tax advice. Nothing in this communication should be construed as tax advice, a solicitation or offer, or recommendation, to buy or sell any security. Any links provided to other server sites are offered as a matter of convenience and are not intended to imply that Wealthfront Advisers or its affiliates endorses, sponsors, promotes and/or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Wealthfront Advisers, Wealthfront Brokerage, and Wealthfront Software are wholly owned subsidiaries of Wealthfront Corporation.

Copyright 2024 Wealthfront Corporation. All rights reserved.