An employee stock purchase plan (or ESPP) can be a very valuable benefit. In general, if your employer offers an ESPP, we think you should participate at the level you can comfortably afford and then sell the shares as soon as you can. This strategy allows you to lock in a return on your contributions while avoiding taking additional risk on your company stock (which may already represent a large chunk of your net worth).

In this post, we’ll show you why this strategy makes sense by answering some basic questions:

- What is an ESPP?

- How does an ESPP work?

- Should you participate?

- How do you make money from an ESPP?

- How are ESPP gains taxed?

- When should you sell the stock you purchase through an ESPP?

What is an ESPP?

An ESPP is a benefit that offers you the opportunity to purchase shares of your employer’s stock at a discount—often up to 15%. You pay for the shares through accumulated payroll deductions.

ESPPs are only available to employees of publicly traded companies. While not all public companies give you the option to participate in an ESPP, many of them do.

How does an ESPP work?

First, you decide what percentage of your paycheck you would like deducted to buy your company stock at a discount. The IRS limits you to a maximum contribution of $25,000 each year, although your employer may cap your contributions at a lower amount or a percentage of your income. Unlike regular 401(k) contributions, your ESPP contributions are withheld from after-tax income (similar to how Roth 401(k) plan contributions work).

Once you enroll, your payroll contributions accrue during what’s known as the offering period. Your offering period will be broken up into purchase periods, which are generally six months long. At the end of these purchase periods, your employer uses your accumulated contributions to buy shares for you at a discount. For example, you could have a one-year offering period starting on January 1, 2022 with two six-month purchase periods: one ending on June 31, 2022 and the second ending on December 31, 2022. Your shares get purchased on the last day of the purchase period.

Crucially, many plans also have a “look back” provision which makes them even more attractive. Typically, a look back provision allows you to apply whatever discount your employer offers to the lower of two numbers: the price on the first date of the offering period or the price on the last day of the purchase period. A 15% discount on its own is pretty nice, but the ability to apply that discount to the minimum of two prices makes ESPPs even more appealing.

Should you participate in an ESPP?

The short answer is yes, as long as you can afford it. The discount typically justifies participation as long as you can afford to live on the smaller paycheck you’ll receive as a result of your payroll contributions.

How do you make money from an ESPP?

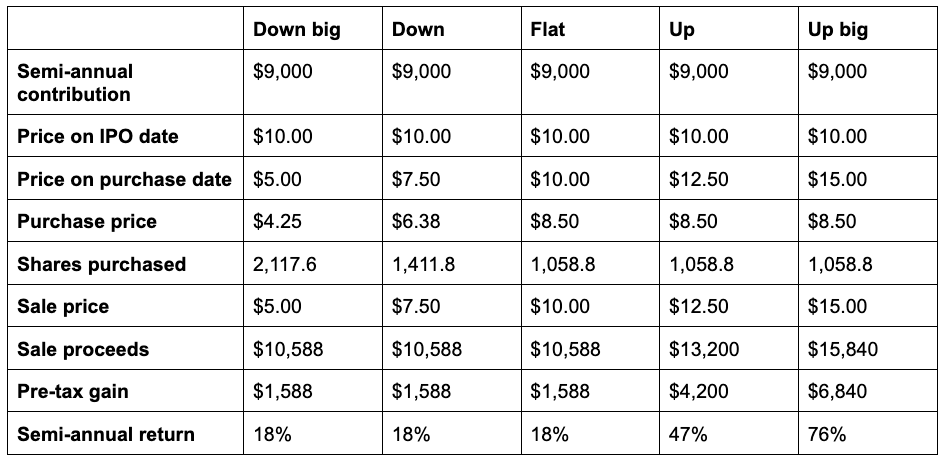

Let’s look at a few different scenarios to show how you can make money from an ESPP. For this analysis, let’s assume your ESPP starts when your company goes public at $10 per share and you’re allowed to invest a maximum of 15% of your pre-tax income (which we’ll assume is $120,000) annually. We’ll further assume your ESPP has a look back provision. That means over the first six-month purchase period, you could invest $9,000 at 85% of the share price either at the beginning or end of the purchase period (whichever is lower).

Here are the scenarios we’ll evaluate:

- Down big: Your company’s stock trades down to $5 per share.

- Down: Your company’s stock trades down to $7.50 per share.

- Flat: Your company’s stock stays flat at $10 per share.

- Up: Your company’s stock trades up to $12.50 per share.

- Up big: Your company’s stock trades up to $15 per share.

The table below shows the possible outcomes over a six-month period, assuming you sell your shares immediately after purchasing them:

Because the discount is taken from the lower of the price on the IPO date and the purchase date, you’d still come out ahead by $1,588 on $9,000 of payroll contributions even if the price was flat, down, or down big. That translates to an 18% pre-tax, semi-annual investment return.

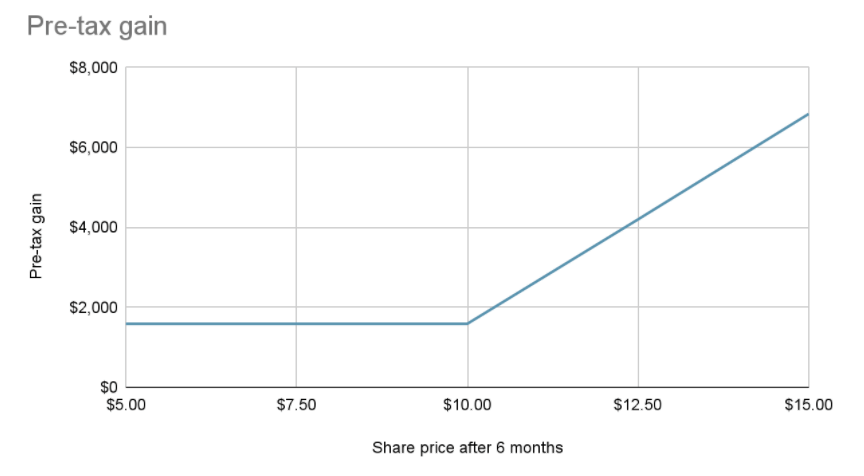

If the stock is up or up big, then you’d benefit significantly more. At $12.50 a share, you’d have a $4,200 gain and at $15.00 a share, your gain would balloon to $6,840. The chart below shows the range of possible outcomes in this example.

In other words, there’s no scenario in this example where you earn less than $1,588 in the first purchase period if you sell on the purchase date.

Now let’s look at what would happen in the second purchase period if your company’s stock was down big in the first half of the year (ending the first purchase period at $5.00 per share) but traded back up to its IPO price ($10 per share) at the end of the year.

If you participated up to the $9,000 max in each of the two purchase periods and sold immediately on each purchase date, then you would generate a pre-tax gain of $1,599 in the first purchase period and $12,176 in the second purchase period (($10.00-$4.25) x $9,000/$4.25). That’s a $13,764 total gain on $18,000 invested, which represents a 76% annual pre-tax return.

Even if the stock closed the 12-month offering period at $9.00 per share (still below the IPO price), you would still earn a gain of $10,059 in the second purchase period. That’s because you’d be able to buy at 85% of the $5.00 share price at the beginning of the second purchase period.

How are ESPP gains taxed?

Your ESPP contributions are taxed as ordinary income, which currently tops out at a marginal rate of 37% at the federal level. If you hold your shares for more than a year after purchasing them AND for more than two years after the beginning of the offering period, then any appreciation above the gain for the discount will be taxed at long-term capital gains tax rates, which currently top out at 20% at the federal level. However, any gains solely attributed to the discount are taxed as ordinary income at the time of sale.

For more detail on how ESPP gains are taxed, check out TurboTax’s resource on the subject.

When should you sell ESPP shares?

It can be tempting to hold onto ESPP stock because of the opportunity to benefit from lower tax rates, but we encourage you to resist the temptation—holding a large position in a single stock can be risky. The stock could decline in value and you could regret your decision.

Instead, we think you should consider using the discount structure to lock in the minimum semi-annual return plus any upside from appreciation, and then sell immediately (on the same day you purchase). If you do this, you typically will get a generous return. You can minimize additional risk by avoiding holding the stock for longer than necessary.

The bottom line on ESPPs

An ESPP with an embedded discount is a great employee benefit. If you can afford it, you should participate up to the full amount and then sell the shares as soon as you can. You might even consider prioritizing your ESPP over 401(k) contributions, depending on your specific financial situation, because your after-tax returns could be higher.

For even more information about equity compensation, check out Wealthfront’s Guide to Equity & IPOs.

Disclosure

The information contained in this communication is provided for general informational purposes only, and should not be construed as investment or tax advice. Nothing in this communication should be construed as a solicitation, offer, or recommendation, to buy or sell any security. Any links provided to other server sites are offered as a matter of convenience and are not intended to imply that Wealthfront Advisers or its affiliates endorses, sponsors, promotes and/or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Intuit, TurboTax and TurboTax Online, among others, are registered trademarks and/or service marks of Intuit Inc. in the United States and other countries. TurboTax is not affiliated with Wealthfront.

Investment management and advisory services–which are not FDIC insured–are provided by Wealthfront Advisers LLC (“Wealthfront Advisers”), an SEC-registered investment adviser, and financial planning tools are provided by Wealthfront Software LLC (“Wealthfront”). Brokerage products and services are offered by Wealthfront Brokerage LLC, member FINRA / SIPC. All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Please see our Full Disclosure for important details.

Wealthfront Advisers, Wealthfront Brokerage and Wealthfront are wholly owned subsidiaries of Wealthfront Corporation.

Copyright 2022 Wealthfront Corporation. All rights reserved.

About the author(s)

Andy Rachleff is Wealthfront's co-founder and Executive Chairman. He serves as a member of the board of trustees and chairman of the endowment investment committee for University of Pennsylvania and as a member of the faculty at Stanford Graduate School of Business, where he teaches courses on technology entrepreneurship. Prior to Wealthfront, Andy co-founded and was general partner of Benchmark Capital, where he was responsible for investing in a number of successful companies including Equinix, Juniper Networks, and Opsware. He also spent ten years as a general partner with Merrill, Pickard, Anderson & Eyre (MPAE). Andy earned his BS from University of Pennsylvania and his MBA from Stanford Graduate School of Business. View all posts by Andy Rachleff