We’ve written before that our Tax-Loss Harvesting service saves Wealthfront clients money when the market is up and when it’s down. But what you might not know is that it renders our high quality investing service basically fee-free by generating tax savings that far outweigh the 0.25% annual advisory fee we charge. According to our research, over 96% of our taxable Automated Investing Account clients have had their advisory fees fully covered by Tax-Loss Harvesting. And over the last five years, Wealthfront clients with a risk score 8 portfolio have enjoyed an average estimated after-tax benefit worth between 6 and 13 times our advisory fee. Tax-Loss Harvesting pays for itself, and it is the primary reason you’re better off investing with Wealthfront instead of trying to do it yourself.

Wealthfront’s Tax-Loss Harvesting in 2020

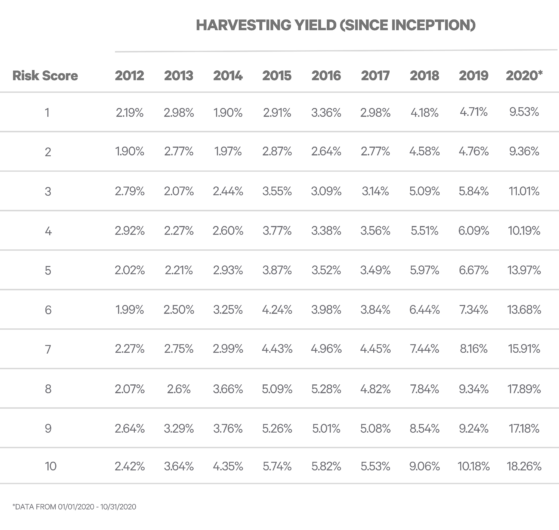

2020 has been an unusually volatile year, and Tax-Loss Harvesting has been a silver lining for our clients. In the table below, we calculated that for the average new client who joined in 2020 (before November 1) with a risk score of 8 (our most common and average risk score), we harvested losses equal to 17.89% of their portfolio value so far this year. This represents an estimated after-tax benefit of 4.47% to 8.95% of their portfolio value depending on their tax rates and ability to use the losses — a staggering 17 to 35 times the 0.25% annual advisory fee we charge.

We got this number by analyzing our service’s annual “harvesting yield,” which takes the amount of harvested losses in a given year and divides that quantity by the portfolio’s value at the beginning of the year. Below, you can see the average annual harvesting yield for each portfolio risk score and “client vintage” (when the client first started using Wealthfront’s Tax-Loss Harvesting). This data includes all losses harvested through October 31, 2020.

As you can see, 2020 has been an exceptionally productive year for our Tax-Loss Harvesting service. However, our software reduces our clients’ taxes in a range of market conditions — not just in years like 2020. For example, even in 2019 when the S&P 500 was up nearly more than 30%, our service paid for itself between 4 and 9 times over.

How much benefit will you get?

There are several factors that play into how much benefit you get from Tax-Loss Harvesting (and, as a result, how many times over your tax savings cover your fee). The timing of your investments makes a difference, as do add-on deposits and the riskiness of your portfolio. The more often you deposit and the higher your risk score, the greater the likely harvesting yield — and thus the likelihood that your tax savings will cover your fees.

The after-tax benefit you receive is a function of your tax rate, so people who live in states with high tax rates get more benefit. For example, if your combined marginal federal and state tax rate is 40% and you have a risk score 8 portfolio that you opened in 2016, then your annual compounded tax savings would have been 2.1% (5.28% harvesting yield x 40%) of your portfolio value. That’s more than eight times the fee we charge, assuming you can use all of your harvested losses that year. A small percentage of our clients (under 4%) have not had their fees covered by Tax-Loss Harvesting. This is most likely to be the case for clients who are in low tax brackets. Having a very low risk score can also make this more likely, as can living in a low-tax state. But even our clients who live in states without a state tax are likely to receive a benefit that is a large multiple of our fee.

Your ability to use harvested losses from year to year might vary depending on the amount of gains you realize, but that’s okay – unused losses just roll over to the following year. You don’t need to realize gains in your portfolio to benefit from tax-loss harvesting, because you can use your losses to offset up to $3,000 in ordinary income each year. Even if you are only able to offset ordinary income with your harvested losses and have no other gains, your tax savings should be a multiple of your advisory fee. The losses our software generates can also be applied to gains on the sale of assets other than securities. For example, if you sell your home, you can use your harvested losses to offset those gains, thus avoiding or reducing a potentially hefty tax bill.

Occasionally, some of the benefit of Tax-Loss Harvesting can be lost due to wash sales. A wash sale occurs when you sell and buy a “substantially identical” security (regardless of what investment portfolio it’s held in) within 30 days. This happens pretty rarely because Wealthfront’s software is designed to avoid wash sales in your Wealthfront accounts. If a wash sale does occur, you just have to wait until the following year to realize the loss.

How does tax-loss harvesting work?

Our Tax-Loss Harvesting service works by selling investments that have declined below their purchase price in value. This sale generates a loss that can be used to offset up to $3,000 of ordinary income each year, along with other taxable gains. Our software then replaces the investment it sold with a highly correlated alternative investment that maintains the risk and return profile of your portfolio. We look for opportunities to harvest tax losses in this manner on a daily basis. It would be inconvenient, if not downright impossible, to do this manually.

Manual tax-loss harvesting is time-consuming because you have to evaluate every tax lot in your portfolio (including reinvested dividends!) every day to take advantage of daily market volatility. It’s a tall order for a human being, but it’s a task perfectly suited to software. Unlike human beings, computers don’t care how many tax lots you have or how often they need to check on those lots, because a computer can scale infinitely.

Tax-loss harvesting isn’t just tax deferral

There’s a common misconception that tax-loss harvesting is just a tax-deferral strategy, rather than a tax savings strategy, and it can make people hesitant to invest with a robo-advisor. Some people mistakenly believe tax-loss harvesting just pushes your taxes down the road and isn’t valuable because you’ll have to pay up eventually. This is wrong for two reasons.

First of all, tax-loss harvesting is a form of tax rate arbitrage. Long-term capital gains are currently taxed at a maximum federal rate of 20%, which is far lower than the highest federal bracket for ordinary income, 37%. Most of the losses we harvest are short-term losses, which can be used to offset short-term gains and ordinary income. When our software sells one of your investments and harvests a loss, it’s true that you are lowering your cost basis which will ultimately increase your gains when you sell your portfolio. But as long as you hold the investment for at least a year, those gains will be taxed at the much lower long-term capital gains rate down the road.

The second reason that tax-loss harvesting isn’t just tax deferral concerns the time value of money. Paying taxes today is more expensive than paying the same amount of taxes in the future because your savings could have been reinvested and thus compounded in the meantime. Because Wealthfront clients are largely young investors who tend not to sell their investments, this compounding effect is especially significant.

The combination of tax-rate arbitrage and the time value of money render tax-loss harvesting incredibly valuable. The present value of the ultimate tax you pay when you liquidate your account should be a small fraction of the taxes you saved along the way with tax-loss harvesting.

Tax savings made simple

We believe in transparency, and that includes publishing the results of our Tax-Loss Harvesting service. We know of no other automated investment service that publishes its harvesting yield which we believe should tell you something about how their performance might compare to ours.

In a wide range of market conditions, our Tax-Loss Harvesting service can harvest significant losses to cover our clients’ advisory fees several times over. Tax-Loss Harvesting is just one piece of Wealthfront’s unparalleled suite of tax-minimization features, and we’re thrilled to offer it to you.

Disclosure

The information contained in this communication is provided for general informational purposes only, and should not be construed as investment or tax advice. Nothing in this communication should be construed as a solicitation, offer, or recommendation, to buy or sell any security. Any links provided to other server sites are offered as a matter of convenience and are not intended to imply that Wealthfront Advisers or its affiliates endorses, sponsors, promotes and/or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Wealthfront Advisers and its affiliates do not provide legal or tax advice and do not assume any liability for the tax consequences of any client transaction. Clients should consult with their personal tax advisors regarding the tax consequences of investing with Wealthfront Advisers and engaging in these tax strategies, based on their particular circumstances. Clients and their personal tax advisors are responsible for how the transactions conducted in an account are reported to the IRS or any other taxing authority on the investor’s personal tax returns. Wealthfront Advisers assumes no responsibility for the tax consequences to any investor of any transaction.

The effectiveness of the tax-loss harvesting strategy to reduce the tax liability of the client will depend on the client’s entire tax and investment profile, including purchases and dispositions in a client’s (or client’s spouse’s) accounts outside of Wealthfront Advisers and type of investments (e.g., taxable or nontaxable) or holding period (e.g., short- term or long-term).

Wealthfront Advisers’ investment strategies, including portfolio rebalancing and tax loss harvesting, can lead to high levels of trading. High levels of trading could result in (a) bid-ask spread expense; (b) trade executions that may occur at prices beyond the bid ask spread (if quantity demanded exceeds quantity available at the bid or ask); (c) trading that may adversely move prices, such that subsequent transactions occur at worse prices; (d) trading that may disqualify some dividends from qualified dividend treatment; (e) unfulfilled orders or portfolio drift, in the event that markets are disorderly or trading halts altogether; and (f) unforeseen trading errors. The performance of the new securities purchased through the tax-loss harvesting service may be better or worse than the performance of the securities that are sold for tax-loss harvesting purposes.

Tax loss harvesting may generate a higher number of trades due to attempts to capture losses. There is a chance that trading attributed to tax loss harvesting may create capital gains and wash sales and could be subject to higher transaction costs and market impacts. In addition, tax loss harvesting strategies may produce losses, which may not be offset by sufficient gains in the account and may be limited to a $3,000 deduction against income. The utilization of losses harvested through the strategy will depend upon the recognition of capital gains in the same or a future tax period, and in addition may be subject to limitations under applicable tax laws, e.g., if there are insufficient realized gains in the tax period, the use of harvested losses may be limited to a $3,000 deduction against income and distributions. Losses harvested through the strategy that are not utilized in the tax period when recognized (e.g., because of insufficient capital gains and/or significant capital loss carryforwards), generally may be carried forward to offset future capital gains, if any.

Investment advisory services are provided by Wealthfront Advisers, an SEC-registered investment adviser, and brokerage products and services are provided by Wealthfront Brokerage LLC, member FINRA / SIPC. Wealthfront Software LLC (“Wealthfront”) offers a free software-based financial advice engine that delivers automated financial planning tools to help users achieve better outcomes.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Please see our Full Disclosure for important details.

Wealthfront Advisers, Wealthfront Brokerage and Wealthfront are wholly owned subsidiaries of Wealthfront Corporation.

© 2020 Wealthfront Corporation. All rights reserved.

About the author(s)

The Wealthfront Team believes everyone deserves access to sophisticated financial advice. The team includes Certified Financial Planners (CFPs), Chartered Financial Analysts (CFAs), a Certified Public Accountant (CPA), and individuals with Series 7 and Series 66 registrations from FINRA. Collectively, the Wealthfront Team has decades of experience helping people build secure and rewarding financial lives. View all posts by The Wealthfront Team