Homeownership has long been a cornerstone of wealth and stability. But for younger generations today, the path to buying a home keeps getting steeper.

Higher interest rates, rising home prices, and a construction shortage are squeezing buyers, and lender practices just make it worse: Bloated sales teams, manual processes, and old technology make getting or refinancing a mortgage needlessly painful and costly. All that inefficiency creates overhead that borrowers ultimately pay for through higher rates and billions in excess fees, pushing homeownership even further out of reach.

We built Wealthfront Home Lending to improve access to homeownership. Just like we used software to modernize investing and cash management so clients can pay less in fees and earn more on their money, we’re now bringing the same approach to mortgages. By building a fully digital product, removing unnecessary steps, and automating away overhead, we aim to consistently offer rates 0.50% or more below the national average while providing a better client experience.

Clients have long requested the “Wealthfront version” of a mortgage, and many already use Wealthfront to save for a home. Our clients collectively own $116 billion in real estate, and in 2025 alone, we sent $2.3 billion in down payment wires. Now, the mortgage process itself happens on the same platform. We’re excited to support digital natives through this major life milestone and help them bring more of their finances together on one trusted platform.

Here’s what you can expect from Wealthfront Home Lending

Thousands of dollars in savings

Affordability is the biggest hurdle in today’s market. Mortgage rates not only impact a buyer’s entry into the market but also their long-term financial health over the life of the loan. We believe mortgage rates should be lower, and with the right technology, they can be.

By automating the high-overhead manual work of traditional firms, Wealthfront Home Lending aims to consistently offer rates 0.50% or more below the national average. For the average new purchaser, that translates to roughly $70,000 in savings over the life of their loan (as of March 31, 2026), leaving more money to invest toward other long-term goals.

Honest pricing, zero surprises

A low rate only matters if it’s the one you actually get. The industry is notorious for “bait-and-switch” rates, but clients will always find transparent, easy-to-understand rates in our product. Our rate calculator gives prospective homebuyers and refinancers a personalized and straightforward estimate in seconds so they can move forward with confidence.

We also charge a one-time, transparent $999 underwriting fee. Lenders have traditionally buried this fee inside a percentage of the total loan amount—0.5% to 1%, which means $2,500 to $5,000 on a $500,000 loan. Ours is flat, upfront, and easy to plan around.

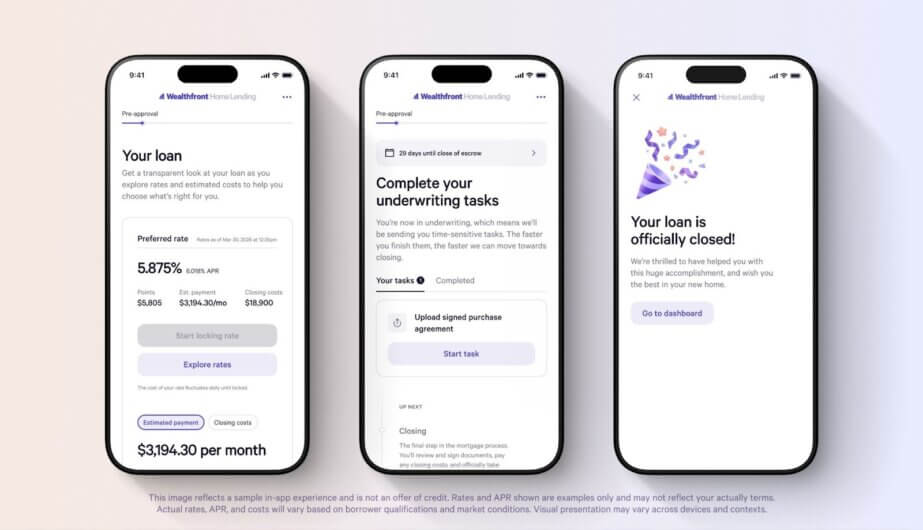

A mortgage experience for digital natives

We’re building the first mortgage product designed to be handled entirely from your phone. Clients can navigate our self-serve application process at their own pace and track their loan process in real time. At the same time, we’ve built a deeply experienced team of loan officers and licensed industry experts who are available by phone and email. And because we have clients’ linked account and income verification data, we expect to dramatically cut down on manually compiling documents.

Beyond just creating a streamlined and intuitive process, we envision creating more value for clients over time through additional automation and innovation. For instance, we’re already building a fast-tracked pre-approval process and personalized in-app decision support to help clients choose the right mortgage, evaluate points, and more. Additionally, we’re working towards a “one-click” refinancing experience for clients with linked mortgages that would make it much easier to lock in a lower rate with very little effort.

The journey ahead for Wealthfront Home Lending

Since our founding, Wealthfront has used technology to improve financial outcomes and deliver more value to our clients. We started in the investing space, and we have since saved clients an estimated $1.5 billion in advisory fees (compared to the 1% traditional advisors typically charge). In that time, we also estimate our Tax-Loss Harvesting has saved investing clients $1.3 billion in taxes. Next, we expanded into cash management: We built a Cash Account that has paid out more than $4.7 billion in interest from program banks in the years since. Now we’re tackling the biggest purchase most of our clients will ever make.

Wealthfront is already profitable, so we don’t need to chase mortgage quotas to stay in business. That frees us up to focus on building the best possible product with competitive rates. It also means clients can trust us to give them guidance that’s right for them, not just for us.

It’s early in our journey to achieve what we envision for Wealthfront Home Lending. While we are already licensed in 26 states, we are rolling out access thoughtfully to ensure the best client experience possible. Currently, our mortgage offering is fully available in Colorado, and we plan to expand access in Texas, California, and other states soon. Check out our website to learn more and see our rates.

Disclosure

All mortgage products are offered by Wealthfront Home Lending, LLC NMLS 2358115

Home loan availability will be subject to credit approval and applicable state and federal licensing requirements. Rates vary based on credit profile, loan terms and market conditions. Not all applicants will qualify for the lowest advertised rates. This communication is for information purposes only and does not constitute a solicitation for a loan or an offer to lend or extend credit. Equal Housing Opportunity.

Wealthfront Home Lending, LLC is an affiliate of Wealthfront Advisers LLC, an SEC-registered investment adviser, Wealthfront Brokerage LLC, Member FINRA/SIPC, Wealthfront Software LLC, Wealthfront Strategies LLC, and the Wealthfront Corporation.

The information contained in this communication is provided for general informational purposes only, and should not be construed as investment, tax, or home lending advice. Interest rates and loan terms reflected are for illustrative purposes only and does not constitute a solicitation for a loan or an offer to lend or extend credit. This is not a commitment to lend. Any links provided to other server sites are offered as a matter of convenience and are not intended to imply that Wealthfront Corporation or its affiliates endorses, sponsors, promotes and/or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

*Rate comparison based on Freddie Mac Primary Mortgage Market Survey® average for 30-year fixed-rate mortgages as of April 6, 2026. Rate available to qualified borrowers meeting the following criteria: 780+ FICO score, $750,000 purchase price, primary single-family residence in Austin, TX, 20% down payment, and payment of 1 discount point. Actual rates may vary. APR and additional terms apply. Not all borrowers will qualify.

Fee Savings Methodology: We first estimated the hypothetical fee a traditional advisor would charge by assuming a 1% advisory fee on assets under management (AUM). This was calculated by taking our total daily cumulative investing AUM across our managed advisory products and multiplying it by the daily effective fee (0.01 / 365) to get the hypothetical total fee amount. Next, we calculated the total fees actually charged by Wealthfront across these managed products, net of any fee waivers. Note: Standalone Direct Indexing accounts were excluded from this analysis because the appropriate comparison is typically the expense ratio of an ETF, not the advisory fee. Similarly, Stock Investing Account and our Automated Bond Ladder were also excluded as their relevant point of comparison is generally not a 1% advisory fee account. The difference between the hypothetical traditional adviser total fees and the actual Wealthfront fees charged for managed advisory products is the estimated client fee savings. This is provided for illustrative purposes only. Actual results or experiences will vary.

Estimated tax savings: We calculated the estimated tax savings based on our clients’ current self-reported income, state of residence, and tax-filing status. From that, we inferred a combined federal and state tax rate (if applicable) for each client. We then multiplied each client’s rate by their harvested losses and added those numbers up to get the $1.3B in estimated tax savings since inception (01/2012) through 02/15/2026. This calculation also assumes that there are enough capital gains to be fully offset by the harvested losses and that current tax laws and rates remain in effect. The actual tax savings realized by any individual client will vary based on their specific tax situation, investment activity, and market performance. These figures are an estimate of potential tax benefits and are not guaranteed. Investors should consult with a tax professional regarding their specific circumstances.

Interest paid out: The total interest figure represents the total amount of interest received by the Cash Account owners over the lifetime of all currently active Cash Accounts. Includes data from 02/14/2019- 02/15/2026. Interest is paid from program banks. The Cash Account, which is not a deposit account, is offered by Wealthfront Brokerage LLC (“Wealthfront Brokerage”), Member FINRA/SIPC. Wealthfront Brokerage is not a bank.

About the author(s)

David Fortunato is Wealthfront’s Chief Executive Officer. He joined Wealthfront in 2009 as the company’s inaugural CTO and was instrumental in launching the company to its first clients in 2011. Previously to his role as CEO, David was the President of Wealthfront. David holds a BS in computer science and economics from Amherst College. View all posts by David Fortunato