As we draw to the close of another year, it’s common for investors to ask themselves, “am I invested the right way for the long term?” Unfortunately, too often we lack access to the data that could help answer that question.

Fortunately, Wealthfront is in a unique position. We have seen what thousands of people’s portfolios looked like before they were transferred to us and reinvested in tax-efficient, low-cost, globally-diversified portfolios. Being a data-driven company, we’ve created metrics to analyze the fees, composition and diversification of the transferred portfolios.

What we see is troubling. Fewer than one in ten of the transferred portfolios were properly built. 92% of the portfolios reviewed were challenged by some combination of high fees, cash drag and poor diversification. These issues could easily leave investors with hundreds of thousands of dollars less over the course of their investing lives.

Based on these common and expensive issues, we created three key questions every investor should ask herself as she enters the new year.

Three Questions You Should Ask about Your Investments

Question 1: How much am I really paying in fees?

Our analysis evaluated three types of fees: advisory fees, transaction fees and product fees. Advisory fees, which traditionally average about 1% of your account balance per year, are the explicit fees charged by a financial advisor. Transaction fees include both commissions for buying and selling investments and various “nickel-and-dime” fees like wire and account transfer fees. Product fees can be the trickiest to calculate and understand. Mutual funds and ETFs can include multiple layers of fees to cover the cost of managing their funds (“Expense Ratios”), marketing the fund (“12b-1 Fees”) and, in certain cases, paying the broker who sold you the fund (“Sales Loads”). By law the details of these fees must be disclosed, but additional complexities like share classes and fee waivers can make it daunting to sift through the details and figure out your true bottom line.

Here’s what we found.

- 30% of investors pay more than 1% annually in advisory fees. This is more than four times what Wealthfront clients pay (not including our benefit of waiving the fee of $5,000 for each friend you invite).

- 26% of investors pay more than 0.10% annually in transaction fees. With commissions trending toward zero, these fees are both unnecessary and expensive, especially when compounded over many years.

- 51% of investors pay more than 0.25% annually in product fees, more than twice what Wealthfront clients pay. The observed product fees are also understated due to the high concentration of individual stocks in the transferred portfolios.

- The bottom line: 36% of investors with advisers pay more than 1.35% annually in total expenses, or one quarter of their expected long-term annual return! Even 33% of accounts without an advisor pay more than 0.75% in total expenses, more than double the all-in cost for Wealthfront clients.

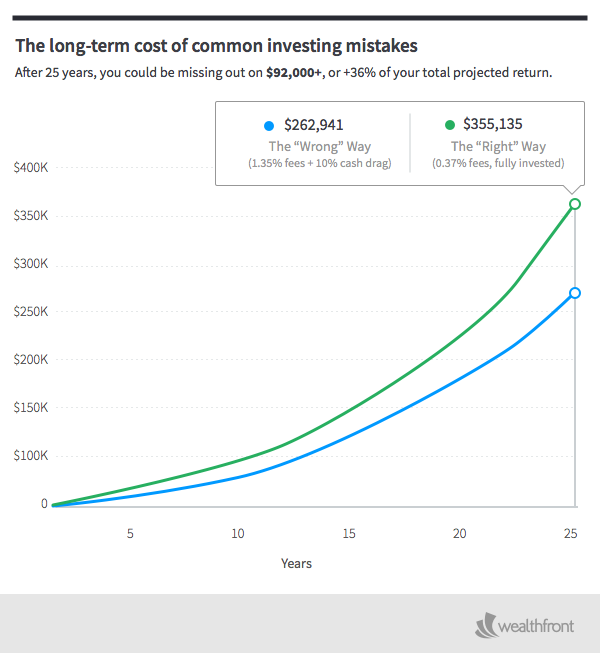

Potential cost: The incremental cost in fees over what you would pay for a Wealthfront account would be 0.98% annually (1.35% – 0.25% Wealthfront advisory fee – 0.12% Wealthfront weighted average ETF management fee). That represents an incremental $74,000 if the fee savings are applied to an initial $100,000 investment compounded at 5.2% (the expected long-term return of an average risk portfolio) over 25 years.

Question 2: Am I holding too much cash?

Holding extra cash beyond an appropriate emergency fund means missing out on significant long-term returns. Cash does not belong in a long term investment portfolio, unless you personally believe, despite vast research to the contrary, that you can beat the market by making short-term, tactical market-timing decisions.

Here’s what we found:

- 35% of investors hold 10% or more of their portfolio in cash. 46% of investors hold more than 5% of their portfolio in cash.

Potential cost: The opportunity cost on holding 10% of an initial $100,000 investment in cash could cost you $25,000 if you invested that cash at a 5.2% annual return over 25 years. Holding 5% of your portfolio in cash could cost you $13,000.

Question 3: Is my portfolio well diversified?

Most investors know that diversifying their portfolios across asset classes and geographies is key to optimizing risk-adjusted returns, yet they often fail to do so. For example, large positions in individual stocks can be exceptionally risky, even if they have performed well in the recent past.

Home bias (the tendency for investors to invest an inappropriately large percentage in stocks from their home country despite the benefits of diversification) also continues to be one of the most consistent mistakes investors make. While US markets have performed exceptionally well recently, it is highly unlikely that this pattern will continue because asset class returns typically revert to their mean. Between 2005-2014, annual returns for US Stocks trailed International and/or Emerging Markets stocks 50% of the time. Poor diversification could be putting your portfolio’s long-term health at risk.

Here’s what we found about the state of people’s portfolios.

- 33% of investors face significant concentration risk, holding the majority of their portfolio in just one or a few individual stocks

- 55% of investors exhibit home bias with more than 95% of their portfolio concentrated in US stocks and bonds

By comparison, the average Wealthfront portfolio with a Risk Score of 7 has exposure to approximately 8,000 stocks, 3,000 bonds and 44 different countries.

Potential cost: The potential cost of poor diversification varies, depending on where your portfolio is concentrated, but individual stocks can lose a significant percentage of their value in a short period of time.

Invest The Right Way for 2016

As 2015 winds to a close, take a moment to evaluate your investment portfolio and ask yourself our suggested questions to make sure you are investing the right way. Our data shows that the majority of investor portfolios can be significantly improved with some simple, straight-forward changes that bring them in line with the best academic theory and investment practices. It’s our hope that armed with these three questions, identifying and fixing these problems will be relatively straightforward.

If you are interested in an automated and effortless way to solve these problems, we encourage you to consider using Wealthfront’s Tax-minimized Brokerage Account Transfer process. Once on board you will also benefit from our unique capability to do Daily Tax-Loss Harvesting and Stock-level Tax-Loss Harvesting – two services that are almost impossible to do yourself.

Disclosure

Nothing in this article should be construed as tax advice, a solicitation or offer, or recommendation, to buy or sell any security. The information provided here is for educational purposes only and is not intended as investment advice. The analysis uses information from third-party sources, which Wealthfront believes to be, however Wealthfront does not guarantee the accuracy of the information. Projected returns do not represent actual accounts and may not reflect the effect of material economic and market factors. Past performance is no guarantee of future results. There is a potential for loss as well as gain. Actual investors on Wealthfront may experience different results from the results shown.

About the author(s)

The Wealthfront Team believes everyone deserves access to sophisticated financial advice. The team includes Certified Financial Planners (CFPs), Chartered Financial Analysts (CFAs), a Certified Public Accountant (CPA), and individuals with Series 7 and Series 66 registrations from FINRA. Collectively, the Wealthfront Team has decades of experience helping people build secure and rewarding financial lives. View all posts by The Wealthfront Team