Introducing the Wealthfront Custodial Account, a simple and flexible way to start investing for your child’s future.

Most investors are well aware that more time in the market typically helps improve returns. So it’s no surprise that this logic is especially impactful for parents wanting to invest for their kids. Today, we’re excited to introduce the Wealthfront Custodial Account, a simple and flexible way to start investing for your child’s future. A Custodial Account allows you to invest on their behalf, setting them up for life expenses beyond education savings, like a down payment or a first car. In addition, the Wealthfront Custodial Account is one of the only Custodial Accounts that’s designed to automatically reduce your child’s future tax burden, before they take ownership of the account.

What are Custodial Accounts for?

A Custodial Account lets you invest on behalf of your child (or any minor) before they take control of the account (as early as 18, but the age of transfer varies by state). The funds can be used for almost anything that benefits your child, whether you withdraw before or after the age of transfer, and there is no annual or lifetime contribution limit. This makes a Custodial Account one of the most flexible ways to support your child financially, no matter how their future unfolds, with more contribution and withdrawal options than a 529 Account or a Section 530A Trump Account.

Custodial Account funds can be used for practically any expense that benefits your child. However, they generally can’t be used for expenses that are considered parental obligations, such as food and shelter. Additionally, though there is no annual contribution limit, regular gift tax limits still apply. For 2026, a donor can gift up to $19,000 per recipient, but anything more than this will need to be reported for tax purposes.

Designed to build long-term wealth and reduce your child’s future taxes

When you open a Custodial Account, we’ll set your child up with a globally diversified portfolio of low-cost index funds designed to soften the impact of the market’s ups and downs. You can choose between three levels of risk; low, medium, or high and our software will automatically keep your portfolio balanced with your preferred risk level. You can also customize your child’s portfolio by adjusting allocations, specific asset classes, and adding specific ETFs.

We’ll even look for opportunities to help lower your child’s future taxes by automatically taking advantage of available tax benefits. For example, children can generally receive up to $1,350 of unearned income (such as interest, dividends, and capital gains) each year without owing federal income tax, though lower filing thresholds may apply in certain states. In addition, another $1,350 of long-term capital gains and qualified dividends may qualify for a 0% federal tax rate, as this portion is taxed at the child’s tax rate. Our software aims to take advantage of these limits by realizing gains when they could be taxed at a low or 0% federal tax rate (assuming your child doesn’t have significant earned income or additional investment income elsewhere).

When gains are realized, the investment’s cost basis increases. A higher cost basis means less taxable gain when the investment is sold in the future (assuming the asset appreciates). As a result, your child may owe less taxes later in life, when they’re more likely to be in a higher tax bracket.

This strategy is known as Tax-Gain Harvesting. If you’re familiar with Tax-Loss Harvesting, it’s a similar concept with a different goal: Tax-Loss Harvesting seeks to reduce taxes in the short term by realizing losses, while Tax-Gain Harvesting seeks to reduce taxes in the future by realizing gains when they can be taxed at a low or 0% federal tax rate. Thus, by resetting the purchase price higher, you can help ensure your child isn’t taxed on that growth in the future.

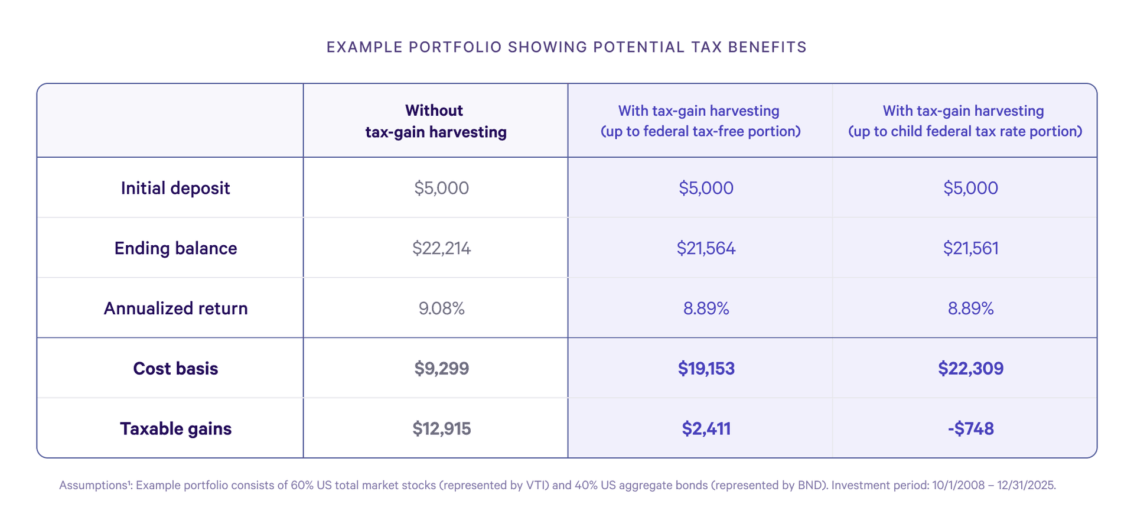

The long-term impact of Tax-Gain Harvesting

Let’s look at an example of Tax-Gain Harvesting at work. Imagine opening a custodial account in 2008, with $5,000 in a simple 60/40 stock/bond portfolio when your child was one year old, and then letting it grow for the next 17 years, until 2025. If you never contributed another dollar, the account could potentially grow to over $21,500 (see table for assumptions). With Tax-Gain Harvesting, our software can sell up to the federal tax-free amount of gains each December, to raise the cost basis. The federal tax-free amount started at $900 in 2008 and increased year over year, to $1,350 by 2025 (and will likely keep increasing in the future to account for inflation). That means your child may only owe federal taxes on $2,411 worth of gains, after an annualized return of 8.89% (if they liquidated the account when they are 18 years old). As illustrated below, this is significantly lower than the account which did not use Tax-Gain Harvesting. For that client, the account would earn a slightly higher annualized return of 9.08%, but the child would owe federal taxes on $12,915. The difference in returns is small, but the client with Tax-Gain Harvesting could help their child save a lot more in taxes!

As we mentioned earlier, our main goal with this feature is to help your child owe as little in future taxes as possible. Let’s also look at another account that took advantage of both the federal tax-free amount and the child’s federal tax rate amount each year. This combined amount started at $1,800 in 2008 and increased year over year, to $2,700 by 2025 (and will likely keep increasing in the future). The account would not owe any federal taxes on gains if they sold the portfolio. In fact, despite growing more than 4x in value, the account would actually incur a small loss, because we would have realized some of the gains when the price was higher than the end of 2025. Doing this on your own would be hard and time-consuming, to say the least. But, as a Wealthfront client, this service is already included in our annual advisory fee—just 0.25%.

Note: If your child receives more than $1,350 in unearned income, like from a savings account or has sizable income from a job, a tax return may be required. Additionally, some states (HI, IN, MO, PA) have a filing requirement that is lower than the federal tax-free limit. We will automatically default to the lower of either the federal tax-free limit or the state filing requirement threshold. However, you can opt out or adjust your Tax-Gain Harvesting limits in the settings.

A great way to help your child learn to invest

In addition to the flexibility of Custodial Accounts, they’re also a great way to teach your child about investing—a way to help them make responsible investing decisions before it becomes theirs to manage. Watching the account grow over time can help them understand how compounding works in practice and a diversified portfolio in particular can illustrate how markets change year to year, busting the myth that an asset class that performs well today will always continue to do so.

Invest for your child, until the account is fully theirs

A Custodial Account is a great choice for parents that want the flexibility to help their child with future life expenses, no matter what path the child ends up choosing. That said, it’s worth remembering that once your child reaches the age of transfer, how they use their funds is up to them. Helping our clients build wealth on their own terms is one of our primary motivations as a company and that includes the next generation, too. A Custodial Account makes this transition easier, for you and for them. And, with the help of our software, making meaningful progress is as easy as watching them grow up.

Disclosure

Investment management and advisory services are provided by Wealthfront Advisers LLC (“Wealthfront Advisers”), an SEC-registered investment adviser. Financial planning tools are provided by Wealthfront Software LLC (“Wealthfront Software”).

The information contained in this communication is provided for general informational purposes only, and should not be construed as investment or tax advice. Nothing in this communication should be construed as a solicitation or offer, or recommendation, to buy or sell any security.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Please see our Full Disclosure for important details.

Custodial accounts (UGMA/UTMA) come with significant limitations. Contributions to a custodial account are irrevocable gifts, meaning once assets are moved into these accounts, they belong to the beneficiary and cannot be reclaimed by the donor for any reason. You also can’t rename the beneficiary or use the assets for another person. Custodians have a fiduciary duty to use funds exclusively for the beneficiary’s benefit. Legal control of the assets automatically transfers to the beneficiary upon reaching the age of termination (typically 18 to 25, depending on the state), at which point they may use the funds for any purpose, regardless of the custodian’’s original intent. These accounts can also negatively impact financial aid eligibility because the assets are owned by the beneficiary. They are weighted more heavily than parental assets in financial aid formulas, which may significantly reduce eligibility for need-based financial aid.

From a tax perspective, Custodial accounts are not tax-deferred; they are subject to “Kiddie Tax” on unearned income above certain thresholds. For the 2026 tax year, the first $1,350 of a child’s unearned income is tax-free, the next $1,350 is taxed at the child’s marginal rate, and any amount over $2,700 is taxed at the parents’ marginal rate. Contributions must adhere to federal gift tax rules ($19,000 for individuals or $38,000 for a married couple in 2026). Any contributions over the gift tax exclusion may be subject to gift tax. Please note that these tax thresholds and gift tax limits are subject to annual adjustments by the IRS and should not be relied upon as permanent. Wealthfront Advisers and affiliates do not provide legal or tax advice and are not liable for tax consequences of client transactions. Please consult a personal tax advisor regarding your individual situation.

529 accounts: You should consult your financial, tax, or other advisor to learn more about how state-based benefits (or any limitations) would apply to your specific circumstances before investing in a 529 plan. You also may wish to directly contact your home state’s 529 plan(s), or any other 529 plan, to learn more about those plans’ features, benefits and limitations. Keep in mind that state-based benefits should be one of many appropriately weighted factors to be considered when making an investment decision. Earnings on nonqualified withdrawals are subject to federal income tax and may be subject to a 10 percent federal tax penalty, as well as state and local income taxes. The availability of tax and other benefits may be contingent on meeting other requirements.

Section 530A Accounts (Trump Accounts) are not available through Wealthfront. They are offered by the US Department of the Treasury, through its designated financial agents. These accounts involve financial risks and structural limitations. Capital is restricted to low fee US index funds or ETFs, which limits asset allocation flexibility and prevents customization. All funds in the account are illiquid and are generally locked with no early withdrawal options until the child reaches age 18. Upon adulthood, the mandatory conversion to a Traditional IRA subjects the capital to retirement regulations; consequently, distributions before age 59 1⁄2 may trigger penalties and ordinary income taxes. Furthermore, these accounts may be subject to political and regulatory risks that could alter tax advantages, match structures, or program rules through future congressional actions or policy shifts. For more information, please visit trumpaccounts.gov.

1The Tax-Gain Harvesting (“TGH”) hypothetical example presented above is intended to demonstrate the potential mechanics of TGH and does not represent the actual results of any specific account. This analysis assumes an initial $5,000 deposit into a static asset allocation of 60% US total market stocks (represented by VTI) and 40% US aggregate bonds (represented by BND) held from 10/01/2008-12/31/2025. This hypothetical example does not reflect the deduction of advisory fees nor the specific impact of rebalancing trades. Actual account performance would be lower if these factors were included, and real-world results may differ significantly due to these and other costs. Market volatility and dividend timing may cause realized gains to differ from projections. Hypothetical returns are not guaranteed, and past performance is not indicative of future results. Indices are not available for direct investment and their performance does not reflect the expenses associated with managing an actual portfolio. This example should not be construed as investment or tax advice. You should consult a qualified tax professional regarding your individual situation.

Tax-Gain Harvesting is intended to help a beneficiary utilize the 0% federal long-term capital gains tax rate available under the Kiddie Tax rules to potentially reduce future federal tax liability. The effectiveness of this strategy is entirely dependent on the beneficiary’s total unearned income for the tax year (this includes any unearned income outside of Wealthfront) and their current qualification under the Kiddie Tax rules (age, any earned income, and student status). For the 2026 tax year, the first $1,350 of unearned income is tax free at the Federal level due to the beneficiary’s standard deduction. Any amount over would trigger a Federal tax filing requirement for the beneficiary (in some cases, it can be included on the parents’ tax return). The next $1,350 of unearned income may be taxed at the beneficiary’s own rate (this will also depend on if it’s long-term capital gains and how much other income the beneficiary may have). Any unearned income above $2,700 is taxed at the parents’ marginal tax rate. The benefit achieved may be limited or eliminated by a client’s specific tax situation. While the strategy aims to realize gains federal-tax-free, state and local taxes may still apply. Wealthfront will harvest less for Clients with beneficiaries residing in states with lower unearned income thresholds to help avoid creating additional state tax filing requirements. The transaction, which involves selling and immediately reinvesting, may result in gains exceeding the client’s selected harvesting limit due to market volatility or late-arriving dividends. Wealthfront Advisers does not provide tax advice. Consult a tax professional for your specific situation.

Diversification and automated investing do not guarantee profit or ensure against loss. Investor experiences can vary widely based on strategies and time horizons. Index funds and ETFs generally offer broad diversification, but may still expose investors to specific market, sector, or asset class risks. Wealthfront provides investment management services but may not achieve returns comparable to those of the general market or specific benchmarks.

Wealthfront Advisers and Wealthfront Software are wholly-owned subsidiaries of Wealthfront Corporation.

© 2026 Wealthfront Corporation. All rights reserved.

About the author(s)

Dave Myszewski is the Vice President of Product at Wealthfront where he oversees product development, consumer research, and client support. Prior to Wealthfront, Dave worked at Apple for 12 years including an engineering role on the first iPhone. Dave holds an MS and BS in Computer Science from Stanford University. View all posts by Dave Myszewski