Hello, and welcome to Vested Interest, a new content series we’re excited to launch about what the latest developments in economics and The Markets might mean for your life, your work, and your money.

The biggest finance stories of the decade so far, arguably, are inflation and the rise of AI. For the average person, inflation has been, well, bad. AI has been a better deal, generating major stock-market gains without displacing jobs en masse — or, at least, without doing that yet. Now the two stories are colliding, with the seemingly unstoppable AI boom actually causing inflation in a key part of the economy. Let’s discuss!

The AI part

You may have noticed that there’s a bit of skepticism growing about how useful AI large-language models have turned out to be for both consumers and businesses. The valuations of companies like Nvidia and Microsoft that are heavily invested in AI have remained high, though; a month ago, Oracle’s share price rose more than 40% in one day on the news that it had signed a $300 billion contract with OpenAI. Why the sustained enthusiasm? Because investors collectively still believe in the future of AI, and are encouraged by the massive amount of capital expenditure, or “capex,” that’s being put into it. In essence, the biggest U.S. corporations are asking investors for permission to spend enormous sums of money on AI research and infrastructure — more than all of Europe spent on defense last year combined, per the Wall Street Journal — and getting that permission in a big way. (Oracle and Open AI’s partnership will involve three huge new data centers.) By some estimates, the U.S. economy’s growth rate would be barely above recession levels if it weren’t for AI buildouts.

The inflation part

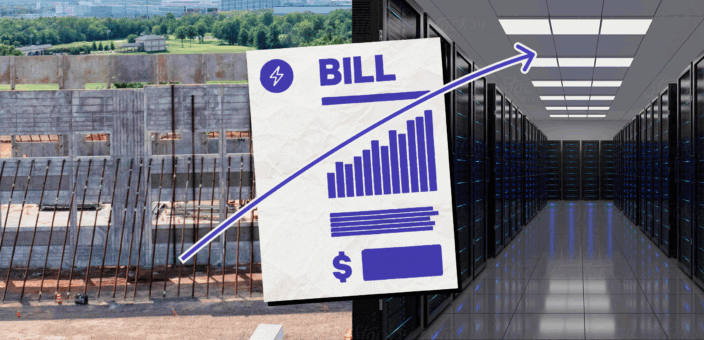

After “Liberation Day,” many observers worried that tariffs imposed by the Trump administration would send consumer prices sharply upward again. It turns out that the prices of goods affected by tariffs haven’t risen that much, but inflation has still remained fairly high because the price of other stuff has been rising — in particular the cost of electricity, which has gone up twice as fast as other consumer costs in the last year.

Why? There are a few reasons, but one of the biggest is… AI capex! Building large language models requires a huge amount of data processing, and all the data centers getting built are essentially warehouses sucking up electricity around the clock. By the Lawrence Berkeley National Laboratory’s estimate, data centers could use as much as one-eighth of all the electricity in the country by 2028. When demand surges like that, the price of keeping the lights on in individual homes does too.

What it means for you

If you were in an eggheaded mood, you might call this a contradiction of pension fund capitalism. That’s a phrase which describes the way a majority of U.S. households, by keeping retirement savings in the stock market, are technically part of the ownership class — and can have financial interests as shareholders that conflict with their interests as workers or consumers. (Trippy!) Or you could just call it a reason to reenact the Alonzo Mourning GIF when you look at your monthly electricity charges; in a way, what you’re paying for is the health of your own portfolio.

But what can you do about it?

The electricity price surge is a reminder of how much day-to-day economic activity is affected right now by beliefs, rather than facts, about the profits AI might eventually generate — and of the logic behind diversification. AI might be a bubble, or it might be a world-changing leap forward. Unless you’re certain you know which is the case, history suggests you’d be well-served to hold investments that are “exposed” to potential AI profits and investments that aren’t. (Luckily, index funds were designed exactly for this purpose – they make it easy to not only diversify across different sectors within the US, but also across other parts of the world and less volatile assets like bonds.)

Disclosure

The information contained in this communication is provided for general informational purposes only, and should not be construed as investment or tax advice. Nothing in this communication should be construed as a solicitation or offer, or recommendation, to buy or sell any security. Any links provided to other server sites are offered as a matter of convenience and are not intended to imply that Wealthfront or its affiliates endorses, sponsors, promotes and/or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Diversification does not guarantee profits or prevent losses. Results vary by strategy and time horizon. Index funds provide broad diversification but can still carry market, sector, or asset-class risks.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Please see our Full Disclosure for important details.

Investment management and advisory services are provided by Wealthfront Advisers LLC, an SEC-registered investment adviser, and brokerage related products are provided by Wealthfront Brokerage LLC, a Member of FINRA/SIPC.

Wealthfront Advisers LLC and Wealthfront Brokerage LLC are wholly owned subsidiaries of Wealthfront Corporation.

Copyright 2025 Wealthfront Corporation. All rights reserved.