The Wealthfront blog has always made a commitment to focusing on data-driven, actionable advice. Sometimes the data challenges conventional financial advice. In this post, we look at the gospel that 401(k) accounts are the best way to save for retirement. As we will explain below, a significant number of investors could even be better off saving money in a taxable, automated investment account with Stock-level Tax-Loss Harvesting and Tax-Loss Harvesting than they would in a 401(k).

For many of you, particularly those who have long advocated for the benefits of 401(k) accounts, this might be hard to accept. However, the data clearly shows that the potential drag from high fees in 401(k) accounts and the powerful tax-deferral benefits of newly available services like Stock-level Tax-Loss Harvesting and Tax-Loss Harvesting can flip conventional wisdom on its head.

How Is This Possible?

For the purposes of this analysis, we’ve made a number of key assumptions.

First, we examined the case of a prototypical Wealthfront client. He or she is part of a young married couple that is living in a high-tax state (California) and earns $260,000 per year on a combined basis. The couple has a combined marginal ordinary income tax rate of 39.2% and has saved at least $100,000.

Second, we assumed our couple would have the same marginal tax rate when they retire as they do today in their early thirties. This could be seen as a controversial position, since many tax planners tell clients that they can expect to be in a lower tax bracket when they retire. We think that is a flawed assumption, and that a default of “same as today” is more likely to be correct for three reasons:

- Tax-Rate Volatility: Actual tax rates are extraordinarily volatile. On a backward-looking basis, a couple earning the equivalent of $260,000 a year would have had a 48% marginal federal tax bracket in 1970, a 59% bracket in 1980, a 28% bracket in 1990 and a 36% bracket in 2000. The question of where tax rates will be in 2045 is a real one, but a default position of “the same as today” seems like your best bet.

- Income At Withdrawal: Less wealthy clients can end up in a lower tax bracket following retirement, as they may have limited retirement savings to draw on. But wealthier clients often experience a side-ways move on income once they start withdrawing money from their retirement plans. Our early-saving, relatively high-income couple is likely to accumulate a sizable nest egg by retirement, so they can expect a relatively high income as well. That means a relatively high tax rate.

- Current Income May Be Low: Couples in their 30s have not yet reached their peak earnings year. For many couples, tax-rates will be on a one-way path upwards from their starting point.

Third, we assumed the 401(k) accounts offered the same breadth of diversification as Wealthfront and therefore the same gross annual returns.

To conduct our analysis, we chose to profile our average client who has a risk score of 7 on a scale of 0 to 10. Based on the expected returns for each asset class as derived from the Capital Asset Pricing Model, we arrive at a gross annual portfolio return of 5.2%. (It’s worth noting that this return includes all Wealthfront fees, and therefore overstates the 401(k)’s likely after fee annual return advantage, because 401(k) plans are known to have much higher fees than Wealthfront. See the section below titled “The Issue with 401(k) Plans? Inferior Investment Choices and High Fees”.)

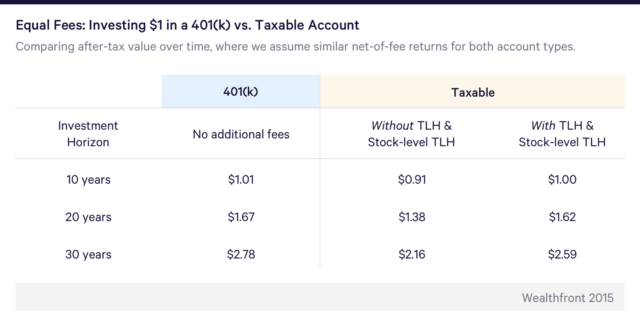

As you can see from the table below, a dollar of savings invested in a 401(k) plan (with no additional fees relative to Wealthfront) will be worth $1.01 in 10 years, $1.67 in 20 years and $2.78 in 30 years.

The after tax account value shows very little gain ($1.01 vs. $1.00) after 10 years because almost all the gain is eaten up by the 39.2% tax you have to pay upon withdrawal. Longer investment horizons have the benefit of more tax-free compounding.

As a result, it is clear that if you assume the same investments and the same fees, a taxable account without Tax-Loss Harvesting or Stock-level Tax-Loss Harvesting is worth a lot less than the 401(k) for each investment horizon ($0.91 vs. $1.01, $1.38 vs. $1.67 and $2.16 vs. 2.78). The addition of Tax-Loss Harvesting and Stock-level Tax-Loss Harvesting makes the numbers a lot closer, but the Wealthfront taxable account is still worth less at the end of each investment horizon.

The Issue with 401(k) Plans? Inferior Investment Choices and High Fees

Unfortunately 401(k) plans are rife with unreasonable fees and inferior investment choices. According to a joint study of Deloitte and the Investment Company Institute, the participant weighted average cost of all 401(k) plans surveyed was 0.73%. 87% of this cost was charged to the investor, so the actual average annual participant cost was 0.64% (0.73% * 87%).

According to The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at 401(k) Plans, the average individual participant cost of the 401(k) plans they surveyed was 0.53%. These fees compare to the all in annual costs for Wealthfront of at most 0.37% (0.25% advisory fee + 0.12% weighted average management fee on ETFs deployed). I say “at most” because Wealthfront manages $5,000 for free for every friend a client invites who signs up for the service. In other words, if a client invests $100,000 then her fee will only be 0.37% (0.25% on $100,000 advisory fee + 0.12% ETF management fee) and a client who invests $200,000 will only incur a total fee of 0.37% (0.25% on $190,000 advisory fee + 0.12% ETF management fee). Using the more conservative Brightscope numbers, Wealthfront’s annual fee advantage vs. the participant-weighted average 401(k) fee ranges from 0.16% (0.53% – 0.37%) to 0.185% (0.53% – 0.345%).

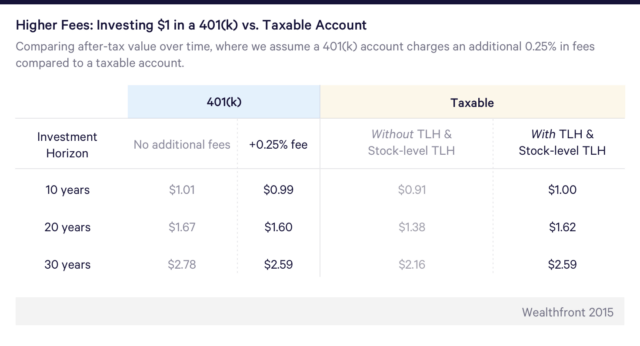

As you can see from the table below an additional 0.25% in fees applied to the 401(k) numbers approximately equates the ultimate Wealthfront after tax account value with the 401(k) account value. Based on these assumptions, a very sizable percentage of the “tax-preferred” 401(k) accounts offered throughout corporate America could be better off if they were invested in a Wealthfront taxable account with Tax-Loss Harvesting and Stock-level Tax-Loss Harvesting.

Please keep in mind participant weighted averages are strongly influenced by lower cost larger plans and represent what the average employee should expect to pay. Our average client is likely to incur much higher 401(k) fees than the participant weighted average because our client base skews young and young people are more likely to work at smaller companies, which have trouble getting a great deal when setting up a 401(k) program.

We encourage you to ask your HR department about the all-in fees on your 401(k) account, and if you’re lucky enough to have a truly low-cost option with great fund choices, you should use it.

Tax-loss Harvesting and Stock-level Tax-Loss Harvesting Assumptions

Clearly this analysis is heavily influenced by the potential impact of Tax-Loss Harvesting and Stock-level Tax-Loss Harvesting. In New Research on the Efficacy of Tax-Loss Harvesting, we presented the annual benefit you could expect from Tax-Loss Harvesting given different investment horizons and different liquidation scenarios. To be consistent with the way we treated 401(k) withdrawals, we used the full liquidation scenario numbers from that post for Tax-Loss Harvesting and the same realized percentage upon full liquidation for Stock-level Tax-Loss Harvesting on a $100,000 portfolio.

The annual after tax benefits of Tax-Loss Harvesting listed in the above referenced blog post include the benefit of tax rate arbitrage and compounding annual savings, so we did not compound the annual tax benefit from these tax minimization strategies in our analysis. Our clients’ actual realized benefit from Tax-Loss Harvesting over our first three years of offering the service has exceeded the numbers we used in our analysis.

Other Factors: Employer Matching Contributions, High Returns and Rollover Penalties

This analysis does not apply if your employer matches your contribution into its 401(k) plan. You should always take your employer up on a dollar-for-dollar or 50-cents-on-the dollar match. There is no better deal on the planet. Our analysis is only appropriate for your non-matched funds.

Moreover, this analysis does not apply if you believe the market will deliver significantly more than a 5.2% return for an average level of risk. If you expect the market to compound at 8% per year, as many static 401(k) models do, the 401(k) will win out. Unfortunately, current index based ETF options and the Capital Asset Pricing Model suggest that achieving an annual 8% return over the long term in a reasonable risk portfolio could be very tricky.

Our analysis also assumed an investment of $100,000 because that is the amount required to gain access to our Stock-level Tax-Loss Harvesting service, which could add 0.20% to your annual after tax return. The amount of fee differential required to justify investing less than $100,000 in a Wealthfront taxable account would therefore have to be 0.45% (0.25% from our analysis + 0.20% lost benefit from Stock-level Tax-Loss Harvesting, not including the fee savings from a smaller account).

You should not convert a 401(k) account from an old employer to a Wealthfront taxable account. This will cause you to incur a 10% penalty for early withdrawal. Rather you would likely be better off rolling it over into a Wealthfront IRA account because you will be charged lower fees and be offered a better diversified portfolio than what you likely are offered in even the best 401(k) plans.

Many advisors recommend investments in 401(k) plans because of the enforced discipline that comes with an account that incurs large penalties if you try to withdraw before a common retirement age. We’d like to believe our readers are intelligent people who don’t need penalties to encourage the appropriate saving behavior.

Liquidity Matters Too

The taxable account has some additional benefits that can be hard to quantify. For example, there is no annual contribution limit on a taxable account. Unfortunately you are limited to contributing only $18,000 per year to a 401(k).

We are huge fans of liquidity. You never know when you’ll need it and unfortunately you often need it when it’s not available. For this reason we would always choose the taxable account over the 401(k) account if the returns are close after considering the fee/performance penalty associated with the 401(k) plan. It’s hard to put a value on liquidity until you need it, but its value is considerable.

Innovation Has Led to Multiple Tax Deferral Paths

In the past, effective tax deferral was only available through regulatory structures, like the 401(k). With the development of effective automated strategies, like Tax-Loss Harvesting and Stock-level Tax-Loss Harvesting, many of the same tax-deferral benefits have been brought to taxable accounts, which already had an advantage of better investment choices and lower fees.

We realize this post is controversial. Arguing that you should favor a taxable account over a 401(k) contradicts decades of financial advice. But then again, we believe that automated investment services like Wealthfront represent a discontinuous improvement over the investment options offered over the past few decades.

If you have a 401(k) at work, this post should help you ask the right questions. But however you choose to save for retirement, the most important advice is still the same: keep your fees low, stay diversified and minimize taxes.

Disclosure

Nothing in this article should be construed as tax advice, a solicitation or offer, or recommendation, to buy or sell any security. The information provided here is for educational purposes only and is not intended as investment advice. The analysis uses information from third-party sources, which Wealthfront believes to be, however Wealthfront does not guarantee the accuracy of the information.

Prospective investors should confer with their personal tax advisors regarding the tax consequences of investing with Wealthfront and engaging in a tax strategy, based on their particular circumstances. Investors and their personal tax advisors are responsible for how the transactions in an account are reported to the IRS or any other taxing authority. When Wealthfront replaces investments with “similar” investments as part of the Tax-Loss Harvesting strategy, it is a reference to investments that are expected, but are not guaranteed, to perform similarly and that might lower an investor’s tax bill while maintaining a similar expected risk and return on the investor’s portfolio. Wealthfront assumes no responsibility to any investor for the tax consequences of any transaction.

Projected after tax returns for Wealthfront’s Stock-level Tax-Loss Harvesting and Tax-Loss Harvesting strategies are intended to show only an expected possible outcome based on historical average returns for a typical Wealthfront account. Several processes, assumptions and data sources were used to create an approximation of how Wealthfront’s Tax-Loss Harvesting strategy might have benefited investors in the past, and a different methodology may have resulted in different outcomes. The results of the historical simulations are intended to be used to help explain the possible benefits of the Stock-level Tax-Loss Harvesting and Tax-Loss Harvesting strategy and should not be relied upon for predicting future performance. The results were achieved by means of the retroactive application of a model designed with the benefit of hindsight. The projected returns consider dividend reinvestment, and interest but do not take into consideration commissions, the effect of taxes, changing risk profiles, or future investment decisions. Projected returns do not represent actual accounts and may not reflect the effect of material economic and market factors. There is a potential for loss as well as gain. Past performance is no guarantee of future results. Actual investors on Wealthfront may experience different results from the results shown.

About the author(s)

The Wealthfront Team believes everyone deserves access to sophisticated financial advice. The team includes Certified Financial Planners (CFPs), Chartered Financial Analysts (CFAs), a Certified Public Accountant (CPA), and individuals with Series 7 and Series 66 registrations from FINRA. Collectively, the Wealthfront Team has decades of experience helping people build secure and rewarding financial lives. View all posts by The Wealthfront Team