How do I know my financial advisor is doing the right thing?

The recent significant drop in world financial markets has created a lot of anxiety – especially among people new to investing. In times like these, investors who outsource the management of their investments can’t help but wonder if they chose the right person or firm to manage their money.

The challenge is it’s really hard to tell who is doing a good job when markets decline. The financial press is saturated with two false promises: the promise that there are people who can reliably beat the market, and the promise that there are people who can reliably protect you from a downturn. Despite overwhelming research to the contrary, many people still believe it’s possible to time the market and avoid the downdrafts.

We believe there are a few tell tale signs of advisors who do not know what they are doing in a down market:

- They sell their losers rather than rebalance

- They increase their allocation to cash

- They sell their riskier asset classes

- They don’t harvest losses

Mistake #1: Selling losers rather than rebalancing

One of the most common mistakes for a passive investor (one who invests in funds that track broad market indexes rather than attempting to outperform the market) is to sell her losers. It might temporarily stop the bleeding, but how do you know when to buy back in? The problem with market timing is that you have to be right twice. If the decline is temporary then you miss out on the recovery. This is exactly the scenario that recently played out in 2009, when far too many investors remained in cash during a huge market recovery. The problem is almost no one can predict what the market will do, even though many are paid a handsome salary to try.

Academic research does show that rebalancing a portfolio will enhance your annual return. Rebalancing is the disciplined process of selling your winners and buying your losers. Think of it as forced contrarianism. When applied to a diversified portfolio of index funds, rebalancing sells funds whose percentage of your portfolio exceeds a predetermined threshold and buys more of funds whose percentage of your portfolio falls short a predetermined threshold due to poor relative performance.

Rebalancing forces investors to purchase assets just at the moments when they emotionally are most biased against them, which is why it is such an effective strategy from a behavioral perspective. For example, it might sound crazy to recommend buying more emerging markets stocks at the moment after a greater than 20% drop in the past 12 months, but research clearly shows keeping your portfolio balanced will produce the strongest risk adjusted results over the long term.

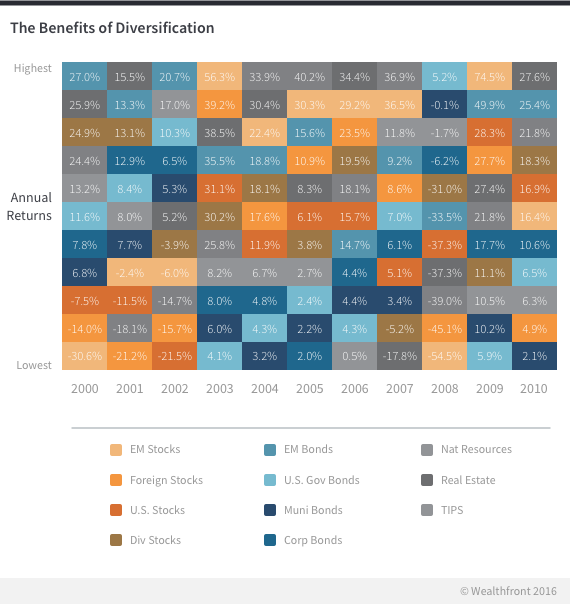

The chart below displays the historic ranking of asset class performance. You can see it might have been unthinkable to sell high performing asset classes in 2000 and 2008 and rebalance into emerging markets, but it turned out that was exactly the right thing to do.

Mistake #2: Increasing your cash allocation

A very common advisor strategy to deal with declining markets is to hold more cash. This is no different from selling a particular asset class. It is premised on the belief that the advisor will know when to reenter the market. Unfortunately, there’s no evidence that investors can consistently time the market. In fact, the research clearly shows the exact opposite is true: investors who attempt to time the market underperform.

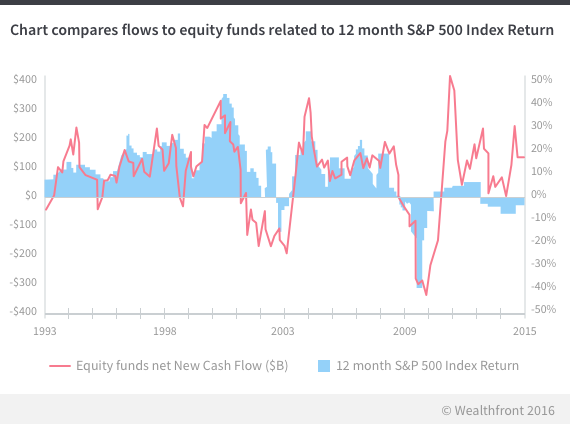

One of the biggest reasons individual investors underperform the markets is they consistently buy when the markets rise and sell when they decline. The chart below illustrates this behavior quite vividly.

DALBAR, a market research firm that has studied this issue over the past 40 years, has found that the average investor underperforms the overall markets by an average of approximately 4% per year due to this bad behavior. Advisors, unfortunately, are not immune from this bad practice, or the negative results it generates over the long term.

Mistake #3: Selling riskier asset classes

One of the best ways to avoid a conversation about how poorly one of your investments performed is to sell the losers. Mutual funds are famous for doing this. The strategy even has a name – window dressing. Mutual funds are able to get away with it because they only report their positions at the end of each quarter. You can’t tell if they had particularly poorly performing individual investments because they often are sold before quarter end and therefore not reported.

Advisors tend to use a different approach when selling off riskier asset classes, which is to convince their clients that they “got out early.” Assuming they didn’t panic at the exact bottom, they can always point to subsequent declines as proof of their prowess. Of course, in the long term, this leads them to the exact type of underperformance DALBAR reports, where they fail to reinvest in the asset class in time for the recovery.

None of these excuses are necessary if you take a passive approach to investing. Markets will go up and down, but in general, if you keep fees low, stay diversified and minimize taxes, your investments will outperform most other investors over the long term.

For example, over the past year, a common question we have heard is “Why not just own the S&P 500?” As you can see from the historical asset class performance chart above, US stocks have done very well on a relative basis of late, but historically asset class performance reverts to the mean, which doesn’t bode well for the S&P 500 in the future. Wealthfront recommends diversifying portfolios across 11 different asset classes, including a significant allocation to emerging markets for our clients with a higher risk tolerance. Last year, owning emerging markets had a significantly negative impact on our average client as compared to a portfolio that only consisted of US stocks.

As our chief investment officer Burt Malkiel explained in How Much Should We Invest in Emerging Markets?, emerging markets stocks now represent over 20% of the world’s aggregate market capitalization. Unfortunately a portfolio allocation of 20% to emerging market stocks would have led to a negative overall portfolio return in 2015 even though the US stock market was up slightly. Emerging markets stocks were down 15.8% in 2015 primarily due to the steep down draft in the Chinese stock market. The 0.1% return from a 30% allocation to US stocks (0.3% return for 2015 * 30% allocation) could not make up for the 3.2% loss that resulted from a 20% allocation to Emerging market stocks (-15.8% return for 2015 * 20% allocation). Your returns would have been much worse if you first invested in the middle of the year.

Over the long term a portfolio diversified according to relative market values should generate the best risk adjusted return because it reflects the global economy – but there can be volatility in the short term. The best advisors deliver their asset allocations based on their clients’ risk tolerance and a mathematical analysis of the risk-adjusted, net of fee, net of tax performance of the actual financial products they utilize. The analysis should consider a variety of historical time periods, and make use of the most academically credible approaches.

Mistake #4: Not harvesting losses

In the case of a portfolio loss, perhaps the most effective way to provide an offsetting economic benefit is through daily tax-loss harvesting. Selling index funds that have traded to a loss and replacing them with the same amount of new index funds that track highly correlated indexes allows you to maintain the risk and return characteristics of your portfolio while realizing a loss that can be applied to up to $3,000 of ordinary income each year and an unlimited amount of capital gains. Your losses can even be carried forward indefinitely.

Unlike “selling your losers” in an attempt to avoid what may be perceived as a bad asset class, tax-loss harvesting maintains your allocation to each asset class consistent with your overall asset allocation and rebalancing goals.

Only automated investment services are able to offer daily tax-loss harvesting because it requires tremendous automation that is only possible through a software-based approach. Some traditional advisors practice year-end tax-loss harvesting, but that approach can miss out on significant opportunities. For example, there was a significant market down draft in June 2013 that allowed Wealthfront to capture losses that could provide tax savings for our clients. The market recovered soon after the down draft and the S&P 500, for example, ended the year up 29.7%. No losses would have been harvested if an advisor waited until year-end.

You are likely missing out on significant improvements to your long term, after tax results if your advisor is taking an ad-hoc or year-end approach to tax-loss harvesting.

Take charge of your investments

Evaluating an advisor’s performance can be difficult, because investors feel like there is no good benchmark against which they can compare their diversified portfolio. The most common mistake people make is to compare their performance against the S&P 500 because it’s the best known index.

The S&P 500 should only be used as a benchmark for US stock performance because it only includes US stocks (and only the 500 largest companies in the US). A diversified portfolio has a much lower risk profile than a portfolio solely comprised of US stocks, so it needs a different benchmark against which it can be compared – if you want an apples to apples comparison.

Interestingly the premier university endowments – the best managed large pools of capital in the world – use something not terribly different from the Wealthfront portfolio as their benchmark. They use mean variance optimization, like Wealthfront, to determine which asset classes they should include and in what mix to maximize their risk adjusted return and then use market indexes to supply the performance for each asset class. The premier universities are able to outperform their benchmark because they have access to alternative assets that normal individuals don’t.

Anxiety in volatile markets is normal. But be sure your advisor avoids common mistakes that can be costly for your long-term return.

Disclosure

This blog is not intended as tax advice, and Wealthfront does not represent in any manner that the outcomes described herein will result in any particular tax consequence. Prospective investors should confer with their personal tax advisors regarding the tax consequences based on their particular circumstances. Wealthfront assumes no responsibility for the tax consequences to any investor of any transaction. Investors and their personal tax advisors are responsible for how the transactions in an account are reported to the IRS or any other taxing authority.

When Wealthfront replaces investments with “similar” investments as part of the tax-loss harvesting strategy, it is a reference to investments that are expected, but are not guaranteed, to perform similarly and that might lower an investor’s tax bill while maintaining a similar expected risk and return on the investor’s portfolio. Wealthfront assumes no responsibility to any investor for the tax consequences of any transaction.

Tax loss harvesting may generate a higher number of trades due to attempts to capture losses. There is a chance that Wealthfront trading attributed to tax loss harvesting may create capital gains and wash sales and could be subject to higher transaction costs and market impacts. In addition, tax loss harvesting strategies may produce losses, which may not be offset by sufficient gains in the account and may be limited to a $3,000 deduction against income. The utilization of losses harvested through the strategy will depend upon the recognition of capital gains in the same or a future tax period, and in addition may be subject to limitations under applicable tax laws, e.g., if there are insufficient realized gains in the tax period, the use of harvested losses may be limited to a $3,000 deduction against income and distributions. Losses harvested through the strategy that are not utilized in the tax period when recognized (e.g., because of insufficient capital gains and/or significant capital loss carryforwards), generally may be carried forward to offset future capital gains, if any.

Wealthfront’s investment strategies, including portfolio rebalancing and tax loss harvesting, can lead to high levels of trading. High levels of trading could result in (a) bid-ask spread expense; (b) trade executions that may occur at prices beyond the bid ask spread (if quantity demanded exceeds quantity available at the bid or ask); (c) trading that may adversely move prices, such that subsequent transactions occur at worse prices; (d) trading that may disqualify some dividends from qualified dividend treatment; (e) unfulfilled orders or portfolio drift, in the event that markets are disorderly or trading halts altogether; and (f) unforeseen trading errors. The performance of the new securities purchased through the tax-loss harvesting service may be better or worse than the performance of the securities that are sold for tax-loss harvesting purposes.

Wealthfront only monitors for tax-loss harvesting for accounts within Wealthfront. The client is responsible for monitoring their and their spouse’s accounts outside of Wealthfront to ensure that transactions in the same security or a substantially similar security do not create a “wash sale.” A wash sale is the sale at a loss and purchase of the same security or substantially similar security within 30 days of each other. If a wash sale transaction occurs, the IRS may disallow or defer the loss for current tax reporting purposes. More specifically, the wash sale period for any sale at a loss consists of 61 calendar days: the day of the sale, the 30 days before the sale, and the 30 days after the sale. The wash sale rule postpones losses on a sale, if replacement shares are bought around the same time.

The effectiveness of the tax-loss harvesting strategy to reduce the tax liability of the client will depend on the client’s entire tax and investment profile, including purchases and dispositions in a client’s (or client’s spouse’s) accounts outside of Wealthfront and type of investments (e.g., taxable or nontaxable) or holding period (e.g., short- term or long-term). Except as set forth below, Wealthfront will monitor only a client’s (or client’s spouse’s) Wealthfront accounts to determine if there are unrealized losses for purposes of determining whether to harvest such losses. Transactions outside of Wealthfront accounts may affect whether a loss is successfully harvested and, if so, whether that loss is usable by the client in the most efficient manner.

A client may also request that Wealthfront monitor the client’s spouse’s accounts or their IRA accounts at Wealthfront to avoid the wash sale disallowance rule. A client may request spousal monitoring online or by calling Wealthfront at 844-995-8437. If Wealthfront is monitoring multiple accounts to avoid the wash sale disallowance rule, the first taxable account to trade a security will block the other account(s) from trading in that same security for 30 days.

The S&P 500® (“Index”) is an index of 500 stocks seen as a leading indicator of U.S. equities and a reflection of the performance of the large cap universe, made up of companies selected by economists. The S&P 500 is a market value weighted index and one of the common benchmarks for the U.S. stock market.

The S&P 500 (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Wealthfront. Copyright © 2015 by S&P Dow Jones Indices LLC, a subsidiary of the McGraw-Hill Companies, Inc., and/or its affiliates. All rights reserved. Redistribution, reproduction and/or photocopying in whole or in part are prohibited Index Data Services Attachment without written permission of S&P Dow Jones Indices LLC. For more information on any of S&P Dow Jones Indices LLC’s indices please visit www.spdji.com. S&P® is a registered trademark of Standard & Poor’s Financial Services LLC and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC. Neither S&P Dow Jones Indices LLC, Dow Jones Trademark Holdings LLC, their affiliates nor their third party licensors make any representation or warranty, express or implied, as to the ability of any index to accurately represent the asset class or market sector that it purports to represent and neither S&P Dow Jones Indices LLC, Dow Jones Trademark Holdings LLC, their affiliates nor their third party licensors shall have any liability for any errors, omissions, or interruptions of any index or the data included therein.

About the author(s)

Andy Rachleff is Wealthfront's co-founder and Executive Chairman. He serves as a member of the board of trustees and chairman of the endowment investment committee for University of Pennsylvania and as a member of the faculty at Stanford Graduate School of Business, where he teaches courses on technology entrepreneurship. Prior to Wealthfront, Andy co-founded and was general partner of Benchmark Capital, where he was responsible for investing in a number of successful companies including Equinix, Juniper Networks, and Opsware. He also spent ten years as a general partner with Merrill, Pickard, Anderson & Eyre (MPAE). Andy earned his BS from University of Pennsylvania and his MBA from Stanford Graduate School of Business. View all posts by Andy Rachleff