This year, interest rates reached their highest level since 2007 and are expected to stay relatively high through 2024. This higher-rate economic environment brings excitement but also confusion. You may be asking, “with all of the compelling ways to earn more on my savings, are equities worth the risk?” Thankfully, we have decades of data to help us answer this question. And it may surprise you that the analysis shows it would be foolish to forego equities.

A brief review of interest rate policy

If you’re one of the many people who came of age during the Great Recession in 2008, rates have been low for as long as you can remember. However, the recent zero-interest rate environment is an anomaly when looking back over the past 50 years.

From January 1973 through December 2007, interest rates were above 4.00% more than 80% of the time! The less prevalent periods when rates dipped below 4.00% occurred following financial instability: after persistent higher inflation from 1992 to 1994 and after the burst of the dot-com bubble from 2001 to 2005. Rates have gone to zero only twice in the past 50 years: 2008 after the Great Recession and 2020 after COVID-19. So, as you can see, we can analyze many previous high interest rate periods to understand how different saving and investing strategies performed historically.

What history teaches us about investing through different interest rate periods

While looking backward can’t predict what will happen next, it can shed light on why we believe equities still have a place in a diversified portfolio, regardless of how appealing interest rates might seem. To show this in practice, we analyzed how equities have performed in comparison with bonds and high-yield savings rates throughout a number of time horizons and under several scenarios. Our analysis shows that over the long-term it is better not to give up on equities, regardless of interest rates.

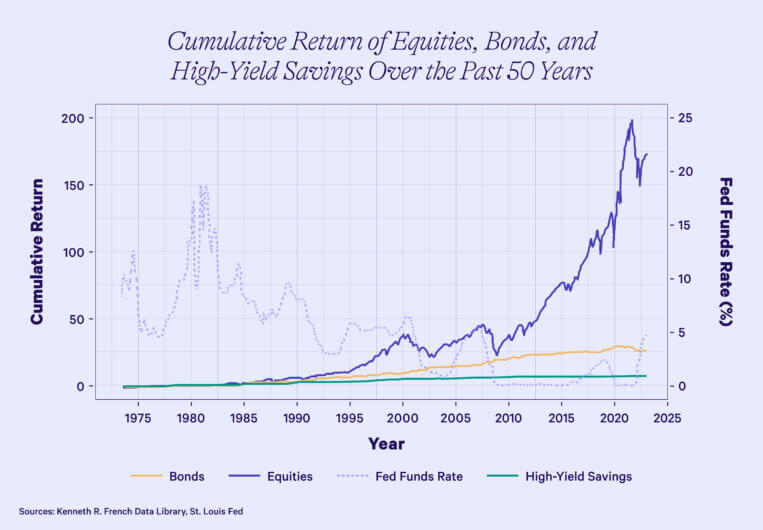

Our first analysis compares how equities, bonds, and high-yield savings rates have performed over the past 50 years (beginning on June 1, 1973, and ending on May 31, 2023). As shown in the below graph, over a longer time horizon, equities consistently and dramatically outperform bonds, which consistently outperform high-yield savings rates.

In our analysis, as described throughout this post, we represented equities using the US total market returns series from Ken French’s website, which includes both large and small-cap US stocks. We represented bonds using 5-year Treasury returns because of their medium time frame, and we represented the high-yield savings rate using 1-month Treasury returns because it is a commonly accepted measure of the risk-free rate and accurately represents the highest available savings yields. (Note that we continue to use the same data sources to represent each category—equities, bonds, and high-yield savings rates—throughout this post).

Given the key principles of investing, this outcome shouldn’t be surprising. A fundamental principle of investing is that for higher risk you have the potential for more reward in the long run. Since high-yield savings accounts are on the lowest end of the risk spectrum in our analysis, followed by bonds offering a medium amount of risk, and equities offering a higher amount of risk, we would also expect the long-term returns to follow that pattern.

How does performance vary between low vs. high-interest rate environments?

Interest rates and bond yields are high right now–does that mean cash and bonds provide a better outcome than stocks? To answer this question, we analyzed how high-yield savings rates, bonds, and equities perform in high versus low-interest rate periods. To do this, any month with an average effective Fed Funds rate higher than 4% over the past 50 years was included in the “High-Interest Rate Period,” and any month lower than 4% was included in the “Low-Interest Rate Period.”

The graphs below show the average annualized return over these High and Low-Interest Rate Periods for stocks, bonds, and high-yield savings in the past 50 years.

It’s clear from this analysis that regardless of whether it was a period of low or high interest rates, on average, equity returns were significantly higher than bonds, and bond returns were considerably higher than high-yield savings rates. When saving rates increased, bonds and equities moved higher as well. The margin of return for equities over bonds and bonds over high-yield savings rates remained similar in both high and low-interest rate periods, with equities outperforming bonds by about 4%, and bonds outperforming high-yield savings rates by more than 2%.

Do higher interest rates mean the end of the 60/40 portfolio?

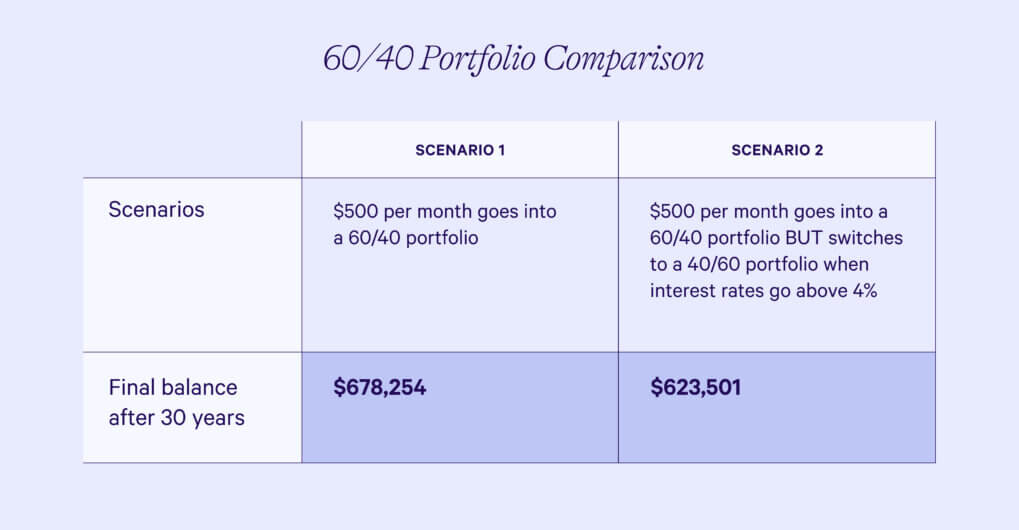

When bond yields increase, there is often an uptick in news headlines predicting the end of the 60/40 portfolio (60% US stocks/40% bonds). Instead, some may advocate for a different mix of asset classes, and one formulation in particular that gains appeal when rates are high is the 40/60 portfolio (40% stocks/60% bonds). Given the attractiveness of today’s bond yields, would it be better to upweight bonds and decrease stocks when rates increase above 4%?

To test this theory, we analyzed the performance of a 60/40 portfolio composed of 60% equities and 40% bonds using the same representative asset classes mentioned above and compared it to a portfolio that upweights those bonds to 60% and down weights those equities to 40% when interest rates go above 4%. To put this analysis in dollar terms, we compared 30-year portfolio return scenarios for investors who we assumed deposited $500 on the last day of each month between May 31, 1993, and May 31, 2023.

Our analysis shows that the 60/40 portfolio comes out ahead even across higher interest rate periods, and investors who chose to upweight bonds would have lost out on nearly $55,000.

How could foregoing equities impact your wallet?

The above analysis makes it fairly obvious that long-term investments in US equities outperformed 5-year Treasury bonds even in high interest rate periods. But given how enticing today’s interest rates are, we wanted to map a few scenarios to show in detail how different allocations to equities, bonds, and high-yield savings could impact your wallet over the long-term.

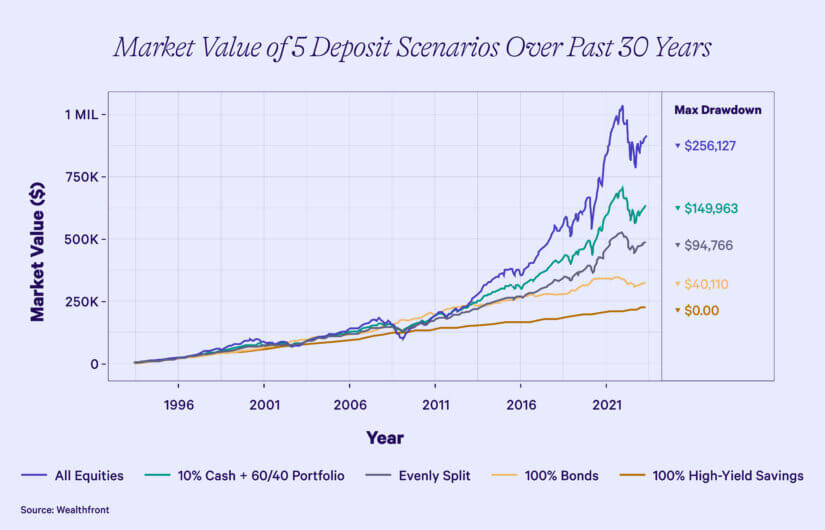

In our analysis, we again focused on the past 30 years and plotted how much someone who started investing on May 31, 1993, would have on May 31, 2023, if they deposited $500 each month between five scenarios with varied percentages in equities, bonds, and high-yield savings:

- Scenario 1: 100% of deposit goes into equities

- Scenario 2: 10% of deposit goes into cash, remainder of deposit goes into 60/40 portfolio

- Scenario 3: Deposit is evenly split: $166.67 goes into equities, bonds, and high yield savings

- Scenario 4: 100% of deposit goes into bonds

- Scenario 5: 100% of deposit goes into high-yield savings

As you’ll see in the analysis, ignoring equities over 30 years could cost hundreds of thousands of dollars in missed opportunities. But by going all in on equities, you’re opening yourself up to much more volatility and, therefore, more risk than the other scenarios. It’s important to view returns in the context of risk, which is why we included the maximum drawdown for each scenario (defined as the maximum loss from peak to trough). The riskiest scenario has a maximum drawdown of over $250,000, while the least risky has a drawdown of $0.

We all want our money to earn more for us, but how much risk is worth it for the extra reward?

Diversification is key for balancing risk and returns

Spreading savings across high, medium, and lower-risk asset classes–also known as diversification–is key to maximizing returns while managing risk. This can be seen clearly in the chart: the line plotting equities shows much larger peaks and valleys than the remaining lines, which include high-yield savings and bonds. And those large valleys are painful: the 100% equities portfolio could have seen a drawdown of a whopping $256,127.

The portfolio that evenly spreads the deposit between all three asset classes is a helpful illustration of the benefits of diversification because it generated almost $170,000 more than a pure bond portfolio but with a much less dramatic drawdown than the scenarios with a higher percentage of equities. By diversifying with lower risk bond and cash assets, the size of the largest drawdown is minimized and continues to flatten out as the percentage of cash and bonds increase.

As we’ve said before, it’s important to think long-term and not let near-term market volatility or headlines influence your strategy. Even as an investment professional, I sometimes find it hard to escape behavioral finance traps, whether it’s seeing the highest bond yields in years or noticing the volatility in my portfolio. But years of analyzing investment data have shown me that the principles of diversification, managing risk, and using the right asset classes according to your particular goals are time-tested strategies for a reason: they continue to prove themselves again and again.

How to save and invest according to your goals

Cash, bonds, and equities all have their place in your portfolio according to your financial objectives. A simple rule of thumb is to think about risk relative to the time spectrum of your needs and goals. The sooner you need to use the funds, the less risk you should be taking. And the farther away your goals, the more risk you can afford to take on in exchange for long-term reward. Below, we break down how to use all three to grow your wealth.

For your “now” money…

Keep your short-term savings safe in a high-yield cash account. Until you’re ready to invest, take advantage of the Wealthfront Cash Account with a high 3.30% APY and up to $8 million of FDIC insurance through our partner banks: that’s 11x the national average savings rate and 32x the amount of FDIC insurance you would get from a traditional bank. Plus, there are no account fees, unlimited withdrawals, $10 wire transfers, and access to a debit card and nationwide network of ATMs so you can easily access your money.

For your “soon” money…

Bond ETFs are ideal for goals in the 1-3 year range. Wealthfront’s Automated Bond Portfolio makes it easy to take advantage of the high yields offered by bonds without sacrificing liquidity. It uses a diversified mix of bond ETFs to provide a higher yield than Treasury bills, CDs, and high-yield savings accounts, more liquidity than I bonds and CDs, and less risk than equities and corporate bonds. It’s an ideal place to save for near-term financial goals like a down payment on a house, an upcoming wedding or vacation, or a home renovation.

For your “later” money…

Use a diversified portfolio of equities for long-term wealth building. Wealthfront’s award-winning Automated Investing Account is a personalized, diversified portfolio of low-cost ETFs designed to help you invest for goals five years away or more. Tailored to your individual risk tolerance, our full suite of automation features minimize the effort of investing and help you balance risk while maximizing after-tax returns. You can even transfer money from your Cash Account to an Automated Investing Account within minutes during market hours.

For your “DIY” money…

If you have additional funds and want to invest in specific companies or ideas, Wealthfront’s Stock Investing Account helps you discover and invest in individual stocks with fractional shares and zero commissions. It comes with access to stock collections created by our Investment Team to help you turn ideas into smart stock investments. You let us know what stocks you want and how much to invest, and we’ll still help you understand how that lines up with your investing goals and manage all the trades on your behalf.

We want to support you as you build long-term wealth in any market condition, and we’re proud to offer you the accounts you need to do just that.

Disclosure

High-yield savings rates are represented by 1-month Treasuries, which serve as a commonly accepted measure of the risk-free rate. This method aligns with established financial models, such as the Fama-French model, where 1-month Treasuries are often used to indicate the risk-free rate. It should be noted that 1-month Treasury rates generally align with the highest rate that banks might provide for high-yield savings accounts.

Bonds are represented by 5-year Treasury returns, which is a frequently quoted rate between shorter-term (<2 years) and longer-term (>10 years) Treasury maturities. Treasuries represent the largest sector in the U.S. bond market. Average market-value weighted maturity for the US Treasury market varies over time, but generally falls between 2 to 10 years. Thus, we used 5-year Treasury returns to represent bonds for simplicity.

The national average interest rate for savings accounts is 0.43% as posted on FDIC.gov, as of July 28, 2023.

We’ve partnered with Green Dot Bank. The checking features offered on your Wealthfront Cash account are provided by and the Wealthfront Visa® Debit Card is issued by Green Dot Bank, Member FDIC, pursuant to a license from Visa U.S.A. Inc. Visa is a registered trademark of Visa International Service Association. Checking features for the Cash Account are subject to identity verification by Green Dot Bank and the Wealthfront Visa® Debit Card is optional and must be requested. Wealthfront products and services are not provided by Green Dot Bank. Green Dot Bank operates under the following registered trade names: GO2bank, GoBank and Bonneville Bank. All of these registered trade names are used by, and refer to, a single FDIC-insured bank, Green Dot Bank. Deposits under any of these trade names are deposits with Green Dot Bank and are aggregated for deposit insurance coverage.

Fee-free ATM access applies to in-network ATMs only. Each calendar month, current eligible clients with ATM Transactions will receive a reimbursement of certain fees associated with their first two out-of-network ATM Transactions. Wealthfront Brokerage will utilize its best efforts to reimburse Green Dot’s $2.50 “out-of-network fee” and up to $5.00 of any operator or owner’s fee for your ATM Transactions, up to a maximum reimbursement of $7.50 per ATM Transaction (the “Reimbursement”). Your maximum total monthly Reimbursement shall be $15.00 ($7.50 + $7.50). If an ATM operator charges fees other than out-of-network fees and/or owner’s fees, Wealthfront Brokerage will not reimburse any portion of those fees. Once the maximum total monthly Reimbursement has been reached, no subsequent out-of-network ATM fees or charges that occur that calendar month will be reimbursed. For full details please review the Out-of-Network ATM Fee Reimbursement Terms and Conditions.Fees and Eligibility requirements may apply to certain checking features, please see the Deposit Account Agreement for details. Copyright 2023 Green Dot Corporation. All rights reserved.

Cash Account is offered by Wealthfront Brokerage LLC (“Wealthfront Brokerage”), a Member of FINRA/SIPC. Neither Wealthfront Brokerage nor any of its affiliates are a bank, and Cash Account is not a checking or savings account. We convey funds to partner banks who accept and maintain deposits, provide the interest rate, and provide FDIC insurance. Investment management and advisory services–which are not FDIC insured–are provided by Wealthfront Advisers LLC (“Wealthfront Advisers”), an SEC-registered investment adviser, and financial planning tools are provided by Wealthfront Software LLC (“Wealthfront”).

The Annual Percentage Yield (APY) for the Cash Account may change at any time, before or after the Cash Account is opened. The APY for the Wealthfront Cash Account represents the weighted average of the APY on the aggregate deposit balances of all clients at the program banks. Deposit balances are not allocated equally among the participating program banks.

The cash balance in the Cash Account is swept to one or more banks (the “program banks”) where it earns a variable rate of interest and is eligible for FDIC insurance. FDIC insurance is not provided until the funds arrive at the program banks. FDIC insurance coverage is limited to $250,000 per qualified customer account per banking institution. Wealthfront uses more than one program bank to ensure FDIC coverage of up to $8 million for your cash deposits. For more information on FDIC insurance coverage, please visit www.FDIC.gov. Customers are responsible for monitoring their total assets at each of the program banks to determine the extent of available FDIC insurance coverage in accordance with FDIC rules. The deposits at program banks are not covered by SIPC.

The information contained in this communication is provided for general informational purposes only, and should not be construed as investment or tax advice. Nothing in this communication should be construed as tax advice, a solicitation or offer, or recommendation, to buy or sell any security. Any links provided to other server sites are offered as a matter of convenience and are not intended to imply that Wealthfront Advisers or its affiliates endorses, sponsors, promotes and/or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Investors may experience different results from the historical analysis shown above. No representation is being made that any client account will or is likely to achieve performance returns or losses similar to those shown herein. Historical analysis is presented for illustrative purposes only. No representation or warranty is made as to the reasonableness of the assumptions made or that all assumptions used in achieving the returns have been stated or fully considered. Changes in the assumptions may have a material impact on the historical analysis presented. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) changes in laws and regulations, and (4) changes in the policies of governments and/or regulatory authorities.

Wealthfront, Wealthfront Advisers and Wealthfront Brokerage are wholly owned subsidiaries of Wealthfront Corporation.

Copyright 2023 Wealthfront Corporation. All rights reserved.

About the author(s)

Fang Rui is a Chartered Financial Analyst (CFA) and an investment researcher at Wealthfront. Prior to Wealthfront, Fang spent nearly a decade at BlackRock where she worked in ETF and index research as well as risk management. She earned a Master of Science in Industrial Engineering and Operations Research from University of California, Berkeley and earned a Bachelor of Science in Engineering with a major in Operations Research and Financial Engineering from Princeton University. View all posts by Fang Rui, CFA