Welcome to our Ask Wealthfront series, where we tackle your questions about personal finance and investing. Want to see your question answered here? Reach out to us on social media and we’ll try to address it in a future column.

How does my risk score at Wealthfront impact my portfolio allocation? How do you keep my portfolio at the right level of risk, and how should my risk score change over time?

In investing, it’s important to get risk right—if you take on too much risk, your portfolio could be too volatile and you might have trouble staying in the market. If you take on too little risk, you could leave potential returns on the table. That’s why Wealthfront uses risk scores to help suggest a portfolio for you based on your risk tolerance. Here’s a closer look at how our risk scores work, how you should (or should not) change them over time, and how we help maintain an appropriate level of risk in your portfolio.

How risk score impacts your portfolio allocation at Wealthfront

When you sign up for an Automated Investing Account, we ask you to take a risk questionnaire that helps assign you a risk score from 0.5 (least risky) to 10 (highest risk). Riskier portfolios have higher expected volatility and higher expected returns, whereas less risky portfolios have lower expected volatility and lower expected returns. Our risk questionnaire is informed by academic research and takes into account three main factors:

- Your age

- Your income and net worth

- Your personal risk tolerance

Together, these pieces of information help us identify and suggest an asset allocation for your needs. Our investing software aims to put clients into portfolios with the highest expected return for their personal risk tolerance and situation. Of course, that looks different for every investor.

A more detailed look at portfolio construction

In addition to your risk score, we also take your tax level and location (whether you live in California or not) into account when we build your portfolio. This means for our Classic portfolios, we actually have seven sets of portfolios:

- Three for taxable non-California accounts (for low, medium, and high tax levels)

- Three for taxable California accounts (for low, medium, and high tax levels) — we have California-specific portfolios because the state has high tax rates and state-specific municipal bond funds, which can be tax-exempt, that meet our criteria

- One for retirement accounts

The same is also true of our Socially Responsible portfolios. Each set of portfolios has dedicated allocations for every risk score, represented by a half point between 0.5 and 10. Portfolios include 5-8 asset classes, and the weighting to each one changes based on risk score and tax level.

The table below shows an overview of how we think about including various asset classes in these portfolios, including high-level tax considerations.

Risk, return, and tax considerations by asset class

| Asset class | Risk level | Potential return | Tax considerations |

| US stocks | High | High | May receive qualified dividends taxed at the capital gains tax rate, which tends to be lower than taxation of ordinary dividends. |

| Foreign developed stocks | High | High | May receive qualified dividends |

| Emerging market stocks | High | High | May receive qualified dividends |

| Dividend growth stocks | High | High | May receive qualified dividends |

| Real estate | High | High | No special tax treatment. Dividends are almost always non-qualified. |

| US corporate bonds | Medium | Medium | No special tax treatment |

| Emerging market bonds | Medium | Medium | No special tax treatment |

| US bonds | Low | Low | In some cases, you won’t need to pay state taxes on US government bonds held within an ETF (subject to some requirements). |

| Municipal bonds | Low | Low | Interest is exempt from federal income tax. Interest is exempt from state income tax IF the bond is issued in the investor’s state of residence. |

| Treasury Inflation-Protected Securities (TIPS) | Low | Low | Interest from treasury bonds is exempt from state income tax. |

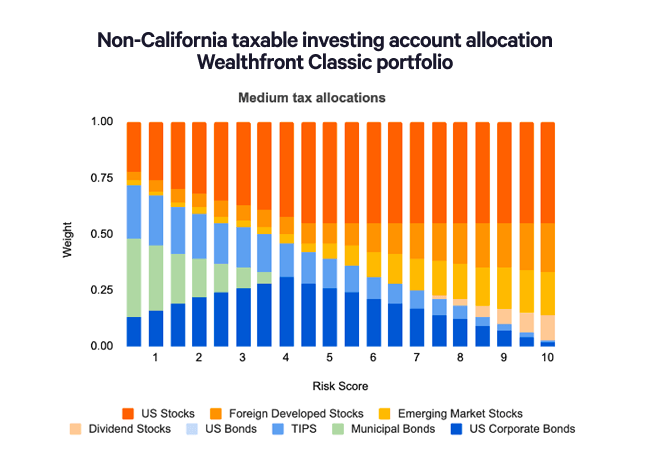

Let’s look at how these considerations play out in a medium tax level, non-California Classic portfolio. The chart below shows the asset allocation for each risk score.

As you can see from this one portfolio set, the allocation to US stocks, foreign developed stocks, and emerging market stocks increases as risk score rises in order to offer higher potential return. If we were to look at a high tax level account, you would see more municipal bonds included due to their federal tax exemption. You can take a closer look at the research behind our portfolio construction here.

How your risk score and asset allocation should change over time

Once you choose a risk score, your target allocation stays the same unless you make changes or we update our portfolio allocations (more on that later). But, it’s a common piece of advice to take on more risk at a younger age, and shift to a more conservative allocation as you get closer to retirement. Some types of investments, like target date funds and our 529s, do this automatically, shifting from a large allocation of stocks to one more heavily weighted towards bonds. What’s the reasoning for this?

- For younger investors: With a longer time horizon, younger investors may choose a higher allocation to growth-oriented investments, which can experience more short-term market fluctuations but could also potentially have a higher return.

- For older investors: Investors nearing retirement may prefer a lower-risk allocation to help reduce the impact of market volatility on funds needed in the near term.

You don’t need to change your risk score all that often

We don’t think there’s any need to change your risk score frequently—in fact, we discourage it. We do think you should update your income and liquid net worth on an annual basis (this helps us calculate a more accurate risk score if you do retake the risk questionnaire). Beyond that, here’s what you should know:

| Good reasons to consider changing your risk score | Bad reasons to consider changing your risk score |

| Big life change that alters your expenses significantlyLarge shift in your incomeLarge shift in your liquid net worth | Market performance—your portfolio is already designed to weather a variety of conditions. Changing your score for this reason is market timing, and it is unlikely to work. |

How we maintain your portfolio’s level of risk over time

There are several things happening behind the scenes to help keep your portfolio at your chosen level of risk:

- Rebalancing: Any investment portfolio’s allocation will naturally drift over time as markets move and some holdings do better than others. When this happens, our software automatically rebalances your portfolio back to its target allocation. Our software is designed to rebalance tax efficiently, using dividends and deposits to help minimize taxable events.

- Regular asset allocation updates: We regularly review and update our portfolio allocations regularly across all risk scores. Our investment research team makes updates to include new research and analysis that aims to improve your portfolio’s expected risk-adjusted return. (For instance, in our last allocation update we added portfolios tailored to your estimated tax level, and adjusted portfolios to help California residents improve their after-tax returns.)

Key takeaways

Risk scores are an important part of how we help build and maintain a portfolio that can help you reach your financial goals. Here are some key takeaways on your risk score at Wealthfront:

- We calculate your risk score using a research-backed questionnaire designed to help you take on an appropriate level of risk for your situation.

- We then use that risk score, in addition to your location and tax level, to suggest an asset allocation.

- Don’t be tempted to change your risk score in response to market conditions—it’s unlikely to benefit you.

- We rebalance your portfolio over time to maintain your level of risk, and we regularly update our asset allocations as a whole.

If you’re curious to learn more about this topic, you can view historical returns by risk score here, or take our risk questionnaire for a more detailed breakdown.

Disclosure

The information contained in this communication is provided for general informational purposes only, and should not be construed as investment or tax advice. Nothing in this communication should be construed as a solicitation, offer, or recommendation, to buy or sell any security. Any links provided to other server sites are offered as a matter of convenience and are not intended to imply that Wealthfront Advisers or its affiliates endorses, sponsors, promotes and/or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Wealthfront Advisers and affiliates do not provide legal or tax advice and are not liable for tax consequences of client transactions. Please consult a personal tax advisor. You are responsible for reporting transactions to the IRS or other taxing authorities.

Diversification and automated investing do not guarantee profit or ensure against loss. Investor experiences can vary widely based on strategies and time horizons. Index funds and ETFs generally offer broad diversification, but may still expose investors to specific market, sector, or asset class risks. Wealthfront provides investment management services but may not achieve returns comparable to those of the general market or specific benchmarks.

Investment management and advisory services are provided by Wealthfront Advisers LLC, an SEC-registered investment adviser, and brokerage related products are provided by Wealthfront Brokerage, a Member of FINRA/SIPC. Financial planning tools are provided by Wealthfront Software LLC. © 2026 Wealthfront Corporation.

About the author(s)

Fang Rui is a Chartered Financial Analyst (CFA) and an investment researcher at Wealthfront. Prior to Wealthfront, Fang spent nearly a decade at BlackRock where she worked in ETF and index research as well as risk management. She earned a Master of Science in Industrial Engineering and Operations Research from University of California, Berkeley and earned a Bachelor of Science in Engineering with a major in Operations Research and Financial Engineering from Princeton University. View all posts by Fang Rui, CFA