KATE & KYLE PARRISH

When Money

Isn't the Goal

For this couple, smart money management is a tool for living the life they want — but is not the ultimate marker of success. This couple prioritizes freedom over consumption, and views the future as an opportunity to leave their mark on the world.

His and hers → theirs

Having open conversations about their finances early on enabled the couple to figure out their shared priorities.

Age

30 and 32

Location

San Francisco

Milestones Achieved

Time Off for Travel

Saving For

Homeownership, Retirement

About a year into dating, they revealed their salaries to each other. "That opened the door," says Kate. "Then, when we moved in together, we really had to look at our finances and build a plan.".

They didn't officially merge finances until they were engaged. At that point, Kyle added Kate to his checking account and credit card, and merged their retirement investments.

"Merging our finances has actually been so much easier than operating separately," says Kyle. "We have a holistic picture of our entire financial model, which makes it easier for us to make decisions together."

One example of what they've been able to accomplish together financially is their year-long around-the-world trip. Kate and Kyle first connected over their mutual love of travel. For years, they steadily put $500 to $1,000 each month into their travel fund. Then, after getting married, they stuck to a $45,000 budget to finance a 12-month journey that spanned six continents and 25 countries. Sticking to a tight budget and thriving while on the road cemented their minimalistic, experiences-over-things money mindset.

Balancing competing priorities

Like many young couples, Kate and Kyle have a variety of big considerations on their minds: like having a baby (at time of writing, Kate is pregnant!), buying a house, and living the lifestyle they want at retirement. To help them prioritize, the couple regularly engages in proactive discussions about what's important to them and regularly assesses progress towards their goals.

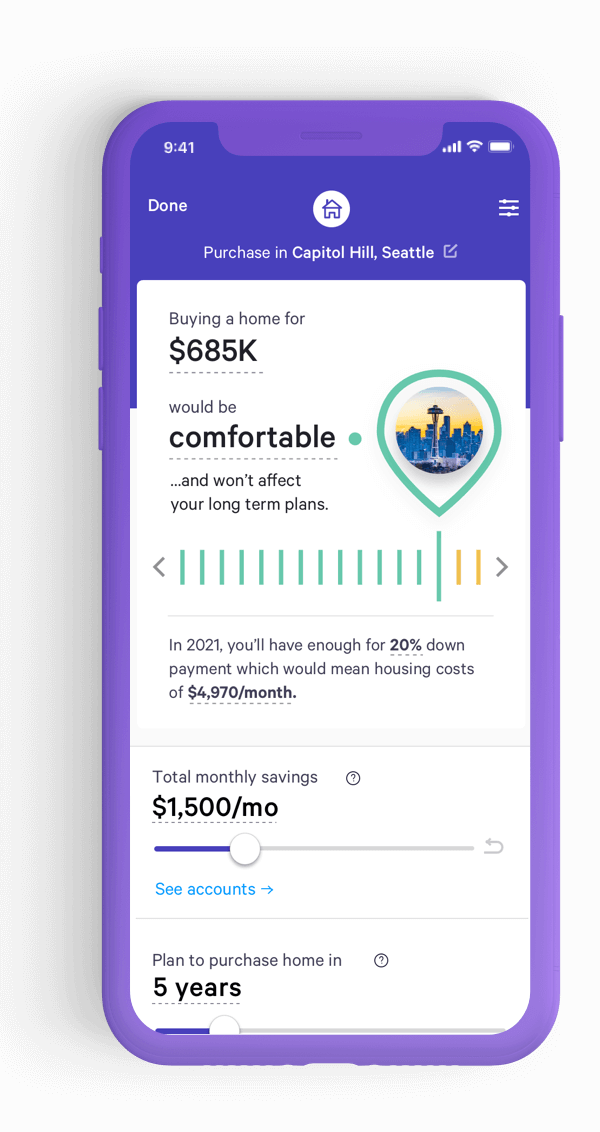

Nine years ago, Kate moved into the two bedroom rent-controlled apartment the couple still occupies today. Now with a child on the way, they're talking more seriously about buying a home and the ideal environment and community they want to be part of long-term. "We've started going to open houses in Marin, where we can imagine one day raising our child — it's suburban but a reasonable commute for work," says Kate.

But they admit that the home prices in the area are intimidating. "Buying a house is very different in the Bay area," says Kyle. "It's hard to get a home for a growing family for under $1 million. It makes everything a lot more complex."

It's more than just the costs. "Owning a home is a big leap into the next phase of our lives. Once you have a hefty mortgage and the added responsibilities that come with a home, you can't turn back," says Kyle.

Instead of rushing to buy, the couple is taking advantage of their rent controlled living situation and socking away money for a bigger down payment down the road. Their plan is to own a home outside the city by the time their child is 2 years old.

"From our travels to other countries, we've seen families live happily in a fraction of the space we have right now, so we have no qualms with staying put for now," says Kyle.

Can I buy a home in this city?

Based on your actual finances, we'll calculate a home budget that reflects the mortgage you'll realistically qualify for while factoring in the all-in costs of homeownership.

Get Started

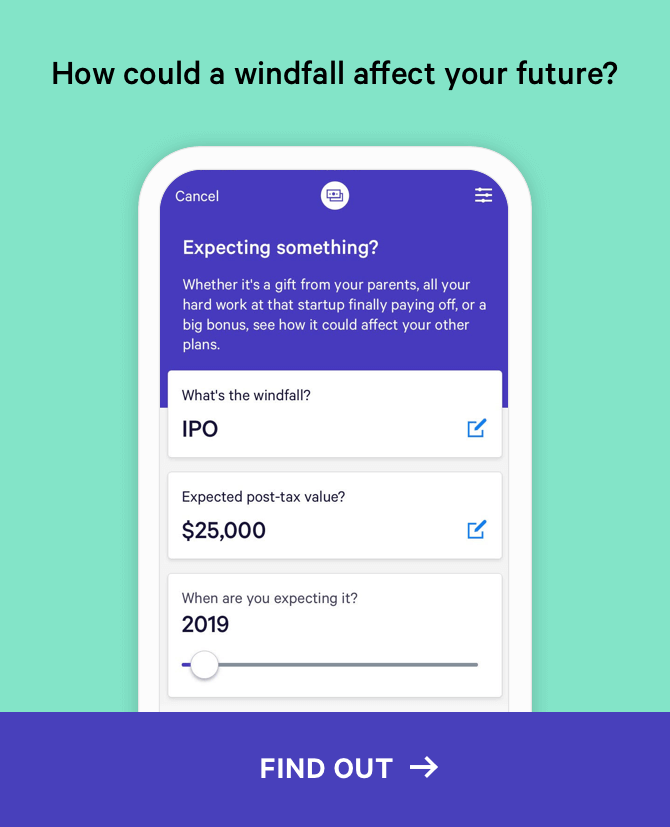

When looking at the couple's overall financial picture, a "very significant part" of their wealth is wrapped up in what every tech worker dreams of: an equity payday. Kyle was an early employee at Dropbox and celebrated the company's IPO in early 2018. Since the shares are now publicly traded, Kyle can sell some or all of his holdings at any time.

While the equity is a blessing, taking action is far from straightforward. Since the company went public, the share price has ranged from $23 to $42. "A drop in share price has a dramatic impact on what the stock can do for our lives," Kyle says.

They have a target share price in mind, and have made the decision to ride it out and wait until the stock reaches that price — but acknowledge that trying to time the market is a risky strategy. Mentally, they've earmarked part of the money for a down payment on a home. "Outside of that, the money gives us peace of mind," says Kyle. "If things went very badly for us financially, we have some protection."

While grateful for Dropbox's success, Kyle regrets not asking for more equity when he was hired. In their current jobs (also startups) the couple took a much more "bullish" approach negotiating their compensation, focusing on stronger equity-to-cash ratios. Given their relatively low cost of living and proven ability to save money, they felt like they could "afford" to opt for more equity over a higher salary. But they're practical with their expectations, and they aren't counting on these equity packages in their longer term financial planning.

Building a meaningful future

Kate and Kyle, 30 and 32 years old, hope to retire when they reach 60.

By having a plan that accounts for future life milestones they feel confident it is a retirement age that is financially feasible. But they don't plan to sit still. They would love to pursue a second career — like opening a boutique hotel, perhaps — while also having the flexibility to live and travel where they choose.

To that end, the couple doesn't keep much money in their checking account. Instead, they move it to their investment accounts, where compounding returns give their cash a much better chance of growing into a healthy nest egg. In total, they allocate 12% of their incomes to their 401(k) plans; a tip Kyle's mentor passed down that he likes to follow.

"It sounds like a lot, but if you live without that cash on a day-to-day basis, you don't even realize you're missing it," says Kyle. "And all of a sudden, when you check in, whether it's six months or five years later, you've amassed a serious amount." While challenging at first, Kyle says investing a high portion of his income early was one of the best financial moves he's ever made.

Since the couple's financial projections are based on their current incomes, they're giving themselves time to build capital.

"We want to spend the next 10 years working and learning and saving," says Kate. "Success will be making that entrepreneurial dream come true — and building our family, finding a way to live off the income we make, and being happy and traveling."

See financial planning at work.

Real clients share how they plan ahead for their futures.